Permanent Establishment in Poland – Complete Guide for Foreign Investors

Expanding into Poland offers significant opportunities for foreign investors, but it also brings complex tax implications that must be carefully managed from the outset. One of the most critical concepts to understand is permanent establishment (PE), as it determines whether your business becomes subject to taxation in Poland – even without setting up a formal legal entity. This guide provides a comprehensive and practical overview of PE in Poland, helping you identify risks, understand obligations, and structure your operations in a tax-efficient and compliant manner.

What is a permanent establishment (PE)?

A permanent establishment (PE) is a fundamental concept in international taxation. It determines whether a foreign company becomes taxable in Poland without formally registering a company.

In simple terms:

A PE arises when a foreign business has a sufficiently permanent and economically significant presence in Poland.

Key characteristics:

- No formal registration is required – a PE may exist even if the foreign company has not set up a legal entity, branch, or office in Poland.

- Based on facts and actual activities – the assessment depends on the real substance of operations (people, functions, assets), not just on contractual arrangements or formal structure.

- Can arise unintentionally – many businesses trigger PE without realizing it, for example through local employees, dependent agents, or operational presence.

- Leads to Corporate Income Tax (CIT) obligations in Poland – once a PE is recognized, the company must calculate and pay tax in Poland on profits attributable to that establishment, along with related compliance requirements.

Why does permanent establishment matter for foreign investors in Poland?

For international companies, PE is often the first and most critical tax question when entering Poland.

If a PE is created, the company may need to:

- Pay Corporate Income Tax (CIT) in Poland – taxation applies to profits attributable to the Polish operations, which must be calculated in accordance with local tax rules.

- Register for VAT – depending on the nature of activities, the company may be required to comply with Polish VAT regulations and reporting.

- Maintain Polish accounting books – proper bookkeeping must be kept in line with Polish accounting standards and tax requirements, at least in Polish and in PLN.

- Run payroll and HR compliance – if employees are involved, the company must handle salaries, social security contributions, and labor law obligations.

- File tax reports and financial statements – regular filings, including tax returns and possibly statutory financial statements, must be submitted to Polish authorities.

This is why PE acts as a gateway trigger for all compliance obligations in Poland, often transforming a simple market entry into a fully regulated tax presence.

Legal framework: Polish law vs OECD standards

The concept of PE in Poland is based on three interconnected layers that must be analyzed together to correctly assess tax exposure:

1. Polish Corporate Income Tax Act (CIT)

This is the primary domestic legislation that defines when and how foreign entities are taxed in Poland. It sets out the basic rules for recognizing income, attributing profits to a PE, and determining tax obligations. However, the domestic definition of PE is often general and must be interpreted in light of international standards.

(Source: Ministry of Finance – CIT rules [1])

2. Double Tax Treaties (DTT)

Poland has concluded a wide network of double tax treaties [3], which play a crucial role in cross-border situations. These treaties define what constitutes a PE, allocate taxing rights between countries, and provide mechanisms to eliminate double taxation. In practice, the treaty definition is often more precise and may limit or expand Poland’s taxing rights compared to domestic law.

3. OECD Model Convention

The OECD Model Tax Convention and its Commentary serve as the key international reference point for interpreting PE rules. They provide detailed guidance on issues such as dependent agents, substance over form, and auxiliary vs core activities [2].

Although not legally binding, they are widely used by tax authorities and courts, especially in ambiguous or borderline cases.

Key principle:

When a double tax treaty applies, its provisions generally take precedence over domestic Polish law. This means that even if Polish regulations suggest that a PE exists, the final determination must always be verified against the relevant treaty, which may override or modify the outcome.

Types of permanent establishment in Poland

Understanding PE requires analyzing different factual scenarios, as a PE may arise in several ways depending on the nature, duration, and substance of business activities carried out in Poland. In practice, tax authorities focus on the economic reality of operations, not just formal structures.

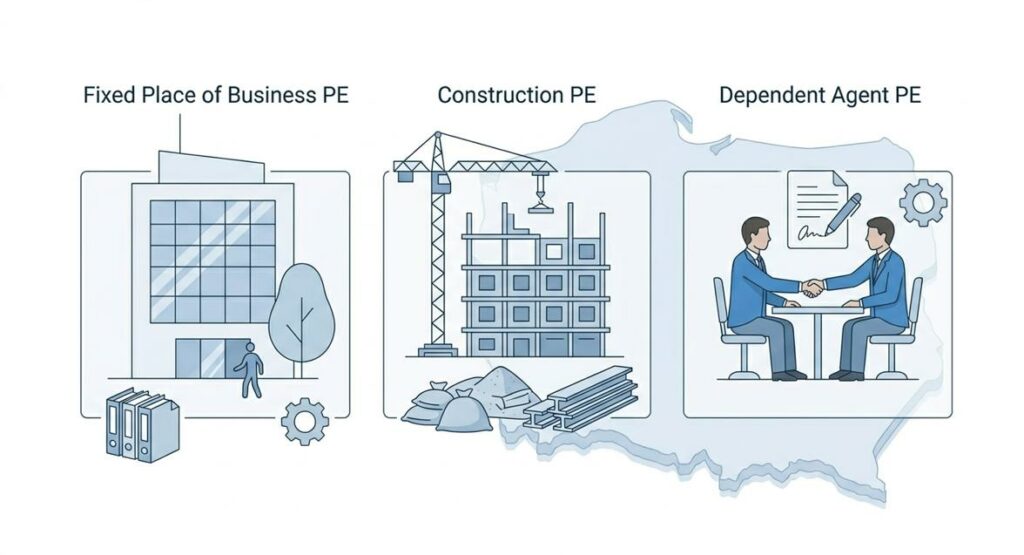

Fixed place of business PE

This is the most traditional and widely recognized form of PE.

A PE arises when a foreign company has a fixed place in Poland through which it conducts its business, regardless of whether the location is owned, rented, or otherwise at its disposal.

Typical examples include:

- Office

- Branch

- Factory

- Workshop

- Warehouse (in certain cases)

Key conditions:

- The place must be physically located in Poland

- It must have a degree of permanence (i.e. not temporary or occasional)

- The business must be carried out through that location

Importantly, even a small or shared space may create a PE if it is used on a continuous basis for core business activities.

Construction PE

A PE may also arise from construction, installation, or assembly projects, even if there is no permanent office or branch.

Key rule:

A construction PE typically arises if the project exceeds 12 months, although this threshold may vary depending on the applicable double tax treaty (sometimes shorter).

Examples include:

Construction sites

Infrastructure or engineering projects

Installation and assembly works

Important considerations:

- The duration of the project is critical

- Time spent by subcontractors may also be included

- Splitting contracts artificially to avoid the threshold may be challenged by tax authorities

Dependent agent PE

Even without any physical presence, a PE can arise through people acting on behalf of the foreign company in Poland.

A PE exists if a person in Poland:

- Acts on behalf of a foreign company

- Has the authority to conclude contracts (or plays a key role in their conclusion)

- Habitually exercises that authority

Example:

A sales representative who negotiates and signs contracts in Poland on behalf of a foreign company

In modern practice, even if the person does not formally sign contracts, PE may still arise if they play a decisive role in the sales process and contracts are routinely approved without significant changes abroad.

In many real-life cases, multiple types of PE may overlap, which is why a detailed, fact-based analysis is always required.

Warehouse and logistics PE (important in practice)

Warehousing is one of the most disputed and practically relevant areas when assessing PE in Poland, especially for e-commerce, distribution, and international supply chains.

While simple storage is often considered an auxiliary activity, the situation changes when the warehouse becomes part of the core business operations.

Key risk factors include:

- Storage combined with sales activity – for example, when goods are stored and sold directly from Poland

- Control over inventory – if the foreign company retains decision-making power over stock, logistics, or distribution

- Local staff managing operations – employees or contractors handling order fulfillment, logistics, or customer service

In practice, the more operational control and business substance is located in Poland, the higher the risk that a warehouse will be treated as a PE.

Important note:

In practice, these categories are not mutually exclusive. A business may simultaneously create a fixed place PE and a dependent agent PE, or combine logistics and personnel presence, which increases overall tax exposure.

Therefore, each case requires a comprehensive, fact-based analysis, taking into account both Polish regulations and applicable double tax treaties.

When permanent establishment does NOT arise

Not every activity performed in Poland leads to the creation of a PE. The law provides for certain exemptions, mainly covering activities of a preparatory or auxiliary nature.

Typical exclusions include:

- Preparatory or auxiliary activities – actions that support the business but are not part of its core revenue-generating function

- Storage of goods only – pure warehousing without involvement in sales or decision-making

- Market research – collecting data without executing business transactions

- Advertising and promotional activities

However, it is important to note that these exceptions are interpreted narrowly by tax authorities. If the activity goes beyond a purely supportive role or becomes economically significant, the exemption may no longer apply.

For a detailed analysis of agency PE risk, see our guide to Dependent and independent agent rules in Poland.

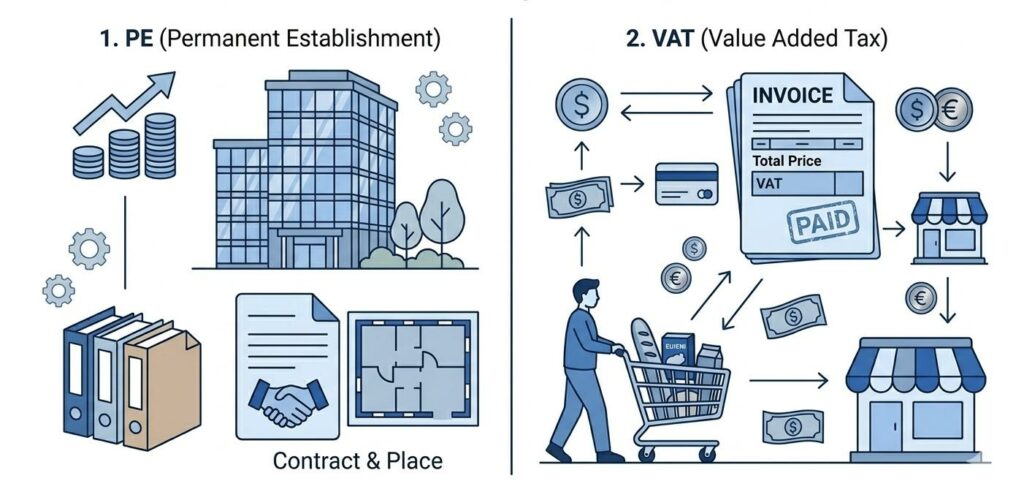

PE vs VAT registration – key differences

A common and critical misconception is that PE is the same as VAT registration – this is not the case.

PE is not equivalent to VAT registration

A company may have VAT obligations in Poland even without creating a PE, for example in cases of:

- Distance sales (B2C cross-border sales)

- E-commerce operations

- Import/export activities

(Source: European Commission – VAT Directive [4])

Key distinction:

- PE impacts income taxation (CIT) – it determines whether business profits are taxable in Poland

- VAT impacts transaction-based taxation – it applies to specific supplies of goods and services

These two areas must be analyzed separately, but always in parallel, as in practice they often overlap and influence compliance obligations [5].

International context – double tax treaties

Double tax treaties play a decisive role in cross-border tax analysis and are essential when assessing PE.

They determine:

- Whether a PE exists in a given jurisdiction

- How profits are allocated between countries

- How double taxation is eliminated (e.g. exemption or tax credit methods)

Practical implication:

The same business activity may create a PE in one country but not in another, depending on the wording of the applicable treaty.

Importantly, a treaty may override or modify the application of Polish domestic law, which is why every PE analysis must include a review of the relevant double tax treaty provisions.

Case studies

Real-life scenarios are essential to understanding how PE rules apply in practice, as outcomes often depend on specific facts and the level of business substance in Poland.

Example 1 – Warehouse operations

A foreign company stores goods in Poland using a third-party logistics provider (3PL).

- If the company has no control over the warehouse, no staff, and the activity is limited to storage → PE is unlikely

- If the company controls inventory, manages logistics decisions, or employs local staff → significant PE risk arises

For a detailed example, see our warehousing case study in Poland.

Example 2 – Sales manager in Poland

A local employee:

- Negotiates contracts with clients

- Signs agreements or plays a decisive role in concluding them

- Acts on a continuous basis

In such a case, the company will most likely create a Dependent Agent PE, even without any physical office in Poland.

Example 3 – Construction project

A foreign company carries out a project in Poland lasting 14 months.

Since the duration exceeds the typical 12-month threshold, a Construction PE arises, triggering tax obligations in Poland.

Risks and tax consequences of a permanent establishment

Failing to properly identify a PE can lead to serious financial and compliance consequences.

Key risks include:

- Double taxation – the same income may be taxed in both Poland and the home country

- Tax penalties – resulting from non-compliance or late registration

- Backdated tax liabilities – authorities may assess tax for prior years

- Transfer pricing issues – incorrect allocation of profits between jurisdictions

Financial consequences:

- Corporate Income Tax (CIT) obligations (19% or 9% – reduced rate).

- Interest on tax arrears

- Additional reporting and documentation requirements

In practice, PE exposure often results in unexpected costs and administrative burdens, especially if identified during a tax audit.

How to assess permanent establishment risk before entering Poland

A proactive and structured approach is critical to avoid unintended tax exposure.

Recommended steps:

- Analyze the business model – understand how revenue is generated and where key functions are performed

- Review contracts and roles – especially authority to negotiate and conclude agreements

- Assess local presence – including people, assets, and functions in Poland

- Check the applicable double tax treaty – to verify how PE is defined and interpreted

- Evaluate VAT exposure – as VAT obligations may arise independently of PE

Best practice:

Conduct a pre-entry tax assessment, ideally with professional advisors, to structure operations in a compliant and tax-efficient way.

How Polishtax supports foreign investors

We provide comprehensive, end-to-end support for companies entering the Polish market, helping them navigate complex tax and regulatory requirements.

Our services include:

- PE risk assessment – identifying whether your planned activities may create a taxable presence

- Tax structuring – designing an optimal and compliant market entry model

- VAT registration and compliance

- Accounting and bookkeeping services in line with Polish regulations

- Payroll and HR compliance, including support for employing staff in Poland

Contact our expert to assess your PE risk and structure your entry into Poland safely.

The article has been prepared based on institutional data and public sources, in accordance with the state of knowledge as of the publication date.

Frequently asked questions (FAQ)

Does hiring an employee in Poland create a PE?

Not always. A PE may arise only if the employee has authority to conclude contracts or plays a key role in generating revenue.

Can a warehouse create a PE in Poland?

Yes, but only in certain conditions. If the warehouse is used beyond storage (e.g. sales or decision-making), PE risk increases.

Is PE the same as a branch?

No. A branch is a legal registration, while PE is a tax concept based on facts.

Do I need to register a company to have PE?

No. PE can arise without any formal registration.

How can I avoid creating PE unintentionally?

You can avoid unintentionally creating a PE by carefully structuring contracts, limiting the authority of local representatives, using independent agents, and conducting a thorough tax analysis before entering a new market.

Bibliography

[1] Internetowy System Aktów Prawnych (ISAP). Polish Corporate Income Tax Act [Ustawa o podatku dochodowym od osób prawnych]. Access date: April 2, 2026. https://isap.sejm.gov.pl/isap.nsf/DocDetails.xsp?id=WDU19920210086

[2] OECD iLibrary. Model Tax Convention on Income and on Capital [Modelowa Konwencja OECD w sprawie podatku od dochodu i majątku]. Access date: April 2, 2026. https://www.oecd-ilibrary.org/taxation/model-tax-convention-on-income-and-on-capital-condensed-version-2017_mtc_cond-2017-en

[3] Podatki.gov.pl (Ministry of Finance). List of Double Tax Treaties (DTT) concluded by Poland [Wykaz umów o unikaniu podwójnego opodatkowania zawartych przez Polskę]. Access date: April 2, 2026. https://www.podatki.gov.pl/podatkowa-wspolpraca-miedzynarodowa/wykaz-umow-o-unikaniu-podwojnego-opodatkowania/

[4] EUR-Lex. Council Directive 2006/112/EC on the common system of value added tax (VAT Directive) [Dyrektywa 2006/112/WE Rady w sprawie wspólnego systemu podatku od wartości dodanej]. Access date: April 2, 2026.

https://eur-lex.europa.eu/legal-content/EN/TXT/?uri=celex%3A32006L0112

[5] OECD iLibrary. Commentary on the Model Tax Convention on Income and on Capital [Komentarz do Modelowej Konwencji OECD]. Access date: April 2, 2026. https://www.oecd-ilibrary.org/taxation/model-tax-convention-on-income-and-on-capital-condensed-version-2017_mtc_cond-2017-en.