Polish Limited Liability Company (sp. z o.o.) 2026

What Is a Polish LLC (Sp. z o.o.) and Why Do 95% of Foreign Investors Choose It?

A Polish limited liability company, known locally as spółka z ograniczoną odpowiedzialnością or sp. z o.o., is the most common corporate vehicle used by foreign investors entering the Polish market. It combines legal personality, limited shareholder liability, relatively low incorporation costs and a flexible management structure. According to business registration practice, the Polish LLC is chosen by approximately 95% of foreign investors because it is easier and cheaper to operate than a joint-stock company while offering stronger separation between the investor and the business than a branch or representative office.

The main advantages of a Polish LLC include limited liability of shareholders, a minimum share capital of only PLN 5,000, access to standard and preferential tax regimes such as 9% CIT and Estonian CIT, no general residency requirement for shareholders or board members, and the possibility of online registration via the S24 system. Polish official business guidance confirms that the minimum share capital of a sp. z o.o. is PLN 5,000 and the nominal value of one share cannot be lower than PLN 50.

|

Criterion |

Sp. z o.o. – Polish LLC |

S.A. – Joint-Stock Company |

Branch of a Foreign Company |

Representative Office |

|

Minimum capital |

PLN 5,000 |

PLN 100,000 |

No separate Polish share capital |

No share capital |

|

Liability |

Company liable with its assets; shareholders generally not liable |

Company liable with its assets; shareholders generally not liable |

Foreign parent company liable |

Foreign parent company liable |

|

CIT in Poland |

Yes, on Polish company income |

Yes, on company income |

Yes, on Polish branch income |

Usually no commercial income allowed |

|

Typical registration time |

2–5 days via S24; longer via notary |

Usually longer and more formal |

Usually several weeks |

Usually several weeks |

|

Best for |

Trading, services, holding, startups, SMEs, foreign investors |

Larger businesses, regulated sectors, capital markets |

Foreign company operating directly in Poland |

Market research, promotion, liaison activities |

Key Facts at a Glance

|

Parameter |

Polish LLC / Sp. z o.o. |

|

Legal form |

Limited liability company in Poland |

|

Polish name |

Spółka z ograniczoną odpowiedzialnością |

|

Common abbreviation |

Sp. z o.o. |

|

Minimum share capital |

PLN 5,000 |

|

Minimum nominal value of one share |

PLN 50 |

|

Standard CIT rate |

19% |

|

Reduced CIT rate |

9% for eligible small taxpayers and qualifying start-ups |

|

Estonian CIT |

0% current CIT on retained/reinvested profits; tax is generally paid upon distribution |

|

Registration route |

Online via S24 or traditional notarial deed |

|

Typical S24 registration time |

Usually 2–5 business days |

|

Typical notarial registration time |

Often 1–2 months, depending on documents and court workload |

|

Residency requirement |

No general Polish residency requirement for shareholders or management board members |

|

Foreign ownership |

100% foreign ownership generally allowed |

|

Accounting |

Full accounting books required |

|

Financial statements |

Annual financial statements filed electronically |

Polish official tax guidance confirms the basic CIT rates and limits, including the standard 19% CIT rate and the reduced 9% CIT rate for eligible taxpayers.

Can a Foreigner Own a Polish LLC? Rules for Non-EU Shareholders

Yes. A foreigner may own 100% of the shares in a Polish LLC, and Polish law does not generally require shareholders or management board members to be Polish residents. This applies in practice to investors from the EU, EFTA, the USA and most non-EU jurisdictions.

For non-EU shareholders, the key distinction is between owning shares and physically managing the company from Poland. Owning shares in a Polish LLC does not itself usually require Polish residency. However, if a foreign board member wants to live in Poland and actively manage the company from Poland, immigration rules, visa requirements, residence permits or work-related formalities may become relevant.

There is one important corporate restriction: a Polish single-shareholder limited liability company cannot be formed solely by another single-shareholder limited liability company. This rule is often overlooked in foreign group structures and should be checked before incorporation.

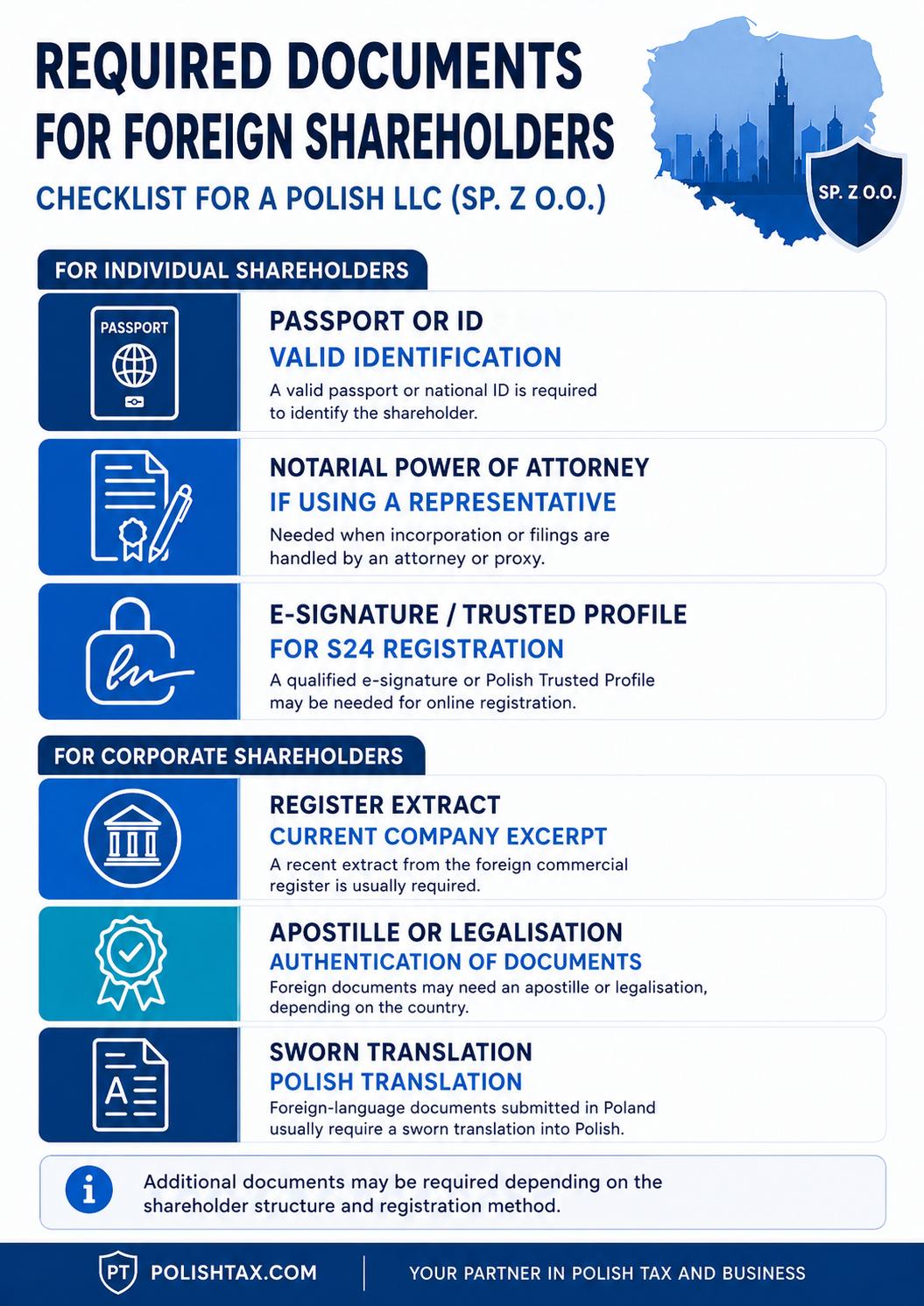

Required Documents for Foreign Shareholders — Checklist

For individual foreign shareholders:

-

Valid passport or national ID card.

-

Personal details: full name, citizenship, address, date and place of birth.

-

Polish PESEL number, if available, but it is not always required for ownership.

-

Notarial power of attorney if the company is incorporated through a representative.

-

Qualified electronic signature or Polish Trusted Profile if using S24 personally.

-

Sworn translation of foreign-language documents, where required.

For corporate foreign shareholders:

-

Current commercial register extract from the foreign company’s jurisdiction.

-

Articles of association or equivalent constitutional document.

-

Details of directors or persons authorised to represent the foreign shareholder.

-

Resolution approving incorporation of the Polish LLC, if required internally.

-

Apostille or legalisation, depending on the country of origin.

-

Sworn translation into Polish.

-

Notarial power of attorney for Polish representatives.

-

UBO data for Polish Central Register of Beneficial Owners reporting.

How to Register a Polish LLC. Step by Step (2026)

-

Choose the structure and shareholders

Estimated time: 1–2 days.

Estimated cost: usually no official fee.

Decide whether the company will have one or several shareholders, who will sit on the management board, and whether foreign corporate documents are needed. -

Choose the company name and business activity codes

Estimated time: 1 day.

Estimated cost: usually no official fee.

The name should not mislead customers and should end with “spółka z ograniczoną odpowiedzialnością” or “sp. z o.o.”. Select appropriate Polish PKD business activity codes. -

Prepare the articles of association

Estimated time: 1–7 days.

Estimated cost: from no separate legal cost in simple S24 cases to legal or notarial fees for customised structures.

In S24, the articles are based on a standard template. For more complex structures, a notarial deed is usually preferred. -

Sign the articles of association

Estimated time: same day if signatures are ready; longer if foreign documents must be legalised.

Estimated cost: electronic signature costs, notarial fees or power of attorney costs may apply.

S24 requires electronic signing. Traditional incorporation requires a Polish notarial deed, either personally or through a representative. -

Pay the share capital

Estimated time: usually before or shortly after registration, depending on structure.

Estimated cost: minimum PLN 5,000 contribution.

Contributions may be in cash or, in notarial incorporation, in-kind contributions may also be possible. -

File the KRS application

Estimated time: same day after signing.

Estimated cost: typically PLN 350 via S24 or PLN 600 via traditional PRS filing.

The company is created upon registration in the National Court Register (KRS). The official business portal confirms that a sp. z o.o. may be incorporated either traditionally by notarial deed or online through S24. -

Obtain tax and statistical numbers

Estimated time: usually automatic after KRS registration, but supplementary filings may be needed.

Estimated cost: usually no major official fee.

The company receives KRS, NIP and REGON numbers, but must file NIP-8 with supplementary data. -

Complete post-registration tax, accounting and compliance steps

Estimated time: 1–4 weeks.

Estimated cost: depends on VAT registration, accounting, UBO filing, bank account and advisory support.

This includes CRBR beneficial owner reporting, VAT-R if needed, accounting setup, KSeF readiness and annual compliance planning.

Online Registration via S24. Fastest Route

The S24 system is the fastest route for registering a Polish LLC online. It is suitable for simple companies with standard articles of association, cash contributions and shareholders or representatives who can sign documents electronically.

To use S24, the signing person must have either a Polish Trusted Profile or a qualified electronic signature accepted by the system. In practice, this may be difficult for foreign founders who do not have a PESEL number or compatible e-signature. In such cases, incorporation through a Polish attorney or traditional notarial incorporation is often more practical.

Typical registration time via S24 is around 2–5 business days, although timing depends on the registry court.

Traditional Notarial Incorporation

Traditional incorporation is used when the company needs customised articles of association, more advanced shareholder rights, in-kind contributions, special transfer restrictions, preferred share arrangements or where the founders cannot use S24.

The articles of association are signed before a Polish notary, either personally or by an attorney acting under a notarial power of attorney. This route is usually more flexible but slower and more expensive. A realistic timeline is often 1–2 months, especially if foreign corporate documents, apostilles and sworn translations are required.

Costs of Setting Up a Polish LLC – Full Breakdown (2026)

|

Cost item |

Typical amount / range |

Notes |

|

KRS and MSiG fee — S24 |

Approx. PLN 350 |

Lower official fee for online incorporation |

|

KRS and MSiG fee — traditional PRS route |

Approx. PLN 600 |

Standard court and publication fee |

|

Share capital |

Minimum PLN 5,000 |

This is company capital, not a registration fee |

|

PCC tax on share capital |

0.5% of share capital |

Usually PLN 25 on the minimum PLN 5,000 capital |

|

Notarial deed |

Depends on share capital and notarial tariff |

Required for traditional incorporation |

|

Notarial copies |

Usually charged per page |

Needed for corporate documentation |

|

Apostille/legalisation |

Depends on country |

Relevant for foreign corporate shareholders |

|

Sworn translations |

Depends on volume and language |

Required for foreign-language documents filed in Poland |

|

Legal or tax advisory |

Depends on scope |

Recommended for foreign shareholders |

|

Accounting setup |

Usually from several hundred PLN monthly |

Full accounting books are mandatory |

|

VAT registration support |

Depends on complexity |

Recommended if the company will trade immediately |

For many foreign investors, the official incorporation fee is only a small part of the total setup budget. The real cost depends on whether the company is simple enough for S24 or whether it requires foreign documents, powers of attorney, sworn translations and tailored articles of association.

Tax Regimes for a Polish LLC in 2026

A Polish LLC is a corporate income tax payer. The main tax regimes available in 2026 are standard CIT, reduced 9% CIT for eligible taxpayers and Estonian CIT for companies that meet the statutory conditions.

Standard CIT – 19% and Reduced 9% Rate

The standard CIT rate in Poland is 19%. A reduced 9% CIT rate may apply to income other than capital gains if the company qualifies as a small taxpayer or starts a new business and meets statutory conditions. In general, the small taxpayer threshold is linked to annual sales revenue not exceeding the equivalent of EUR 2 million, including VAT, in the previous tax year.

The 9% rate applies to income, not revenue, and does not automatically apply to every new company. It may be unavailable in certain restructuring cases or where statutory exclusions apply.

Estonian CIT – 0% on Reinvested Profits

Estonian CIT, formally known as the lump-sum tax on company income, is an alternative taxation model. Its key advantage is that a company generally does not pay current CIT as long as profits remain in the company and are reinvested. Taxation is generally triggered when profits are distributed, for example as dividends.

This makes Estonian CIT attractive for startups, growth companies and businesses that intend to reinvest earnings rather than distribute profits annually. Polish official tax guidance describes Estonian CIT as an alternative form of corporate income taxation, while the applicable lump-sum rates are 10% for small taxpayers or start-ups and 20% for other taxpayers when taxable distribution events occur.

Other Tax Incentives – IP Box, R&D Relief, SEZ

A Polish LLC may also benefit from other tax incentives, depending on its activity:

-

IP Box — 5% preferential taxation for qualifying income from eligible intellectual property rights.

-

R&D relief — additional deduction for qualifying research and development costs.

-

Polish Investment Zone / SEZ-type support — income tax exemption for qualifying new investment projects, subject to a support decision and regional aid limits.

These incentives require proper documentation and should be analyzed before the company starts the relevant activity.

Post-Registration Obligations. What Comes After KRS?

Registration in KRS is only the beginning. After incorporation, a Polish LLC should complete several tax, accounting and compliance steps:

-

File NIP-8 with supplementary tax and organizational data.

-

Confirm NIP and REGON numbers.

-

Register for VAT using VAT-R if required or commercially advisable.

-

Register with ZUS if the company becomes a social security remitter, for example after hiring employees.

-

Open a Polish or EU business bank account.

-

Report beneficial owners to the Central Register of Beneficial Owners.

-

Set up full accounting books.

-

Prepare for KSeF, Poland’s mandatory e-invoicing system.

-

File annual financial statements electronically.

-

File annual CIT returns and keep accounting records.

KSeF is especially important in 2026. According to official KSeF guidance, mandatory issuing of structured invoices applies from 1 February 2026 for taxpayers whose 2024 sales exceeded PLN 200 million including VAT, and from 1 April 2026 for most other taxpayers, with transitional relief for the smallest taxpayers until the end of 2026. Receiving invoices via KSeF is mandatory from 1 February 2026.

Common Mistakes When Setting Up a Polish LLC

Foreign investors most often make the following mistakes when setting up a sp. z o.o. in Poland:

-

Creating an invalid single-shareholder structure

A Polish single-shareholder LLC cannot be incorporated solely by another single-shareholder LLC. This issue should be checked early in group structures. -

Registering too late for VAT

Some companies sign contracts or issue invoices before VAT registration is completed. This may create tax, cash-flow and credibility problems. -

Ignoring KSeF readiness

From 2026, e-invoicing through KSeF becomes a core compliance obligation for companies issuing invoices in Poland. Accounting systems and invoicing workflows should be prepared before the first transactions. -

Choosing the wrong tax office or missing NIP-8 data

Foreign-owned companies may fall under specialised tax offices depending on their profile. Incorrect or late filings may delay practical operations. -

Using a standard S24 template for a complex investment

S24 is fast, but it is not always suitable for joint ventures, investor rights, vesting, drag-along/tag-along clauses or advanced profit distribution rules. -

Not translating or legalising foreign documents properly

Corporate shareholders often need apostilled or legalised register extracts and sworn translations. Missing formalities can delay registration. -

Treating share capital as a cost

The PLN 5,000 minimum share capital is not a government fee. It belongs to the company and can be used for business purposes after incorporation, subject to corporate and accounting rules.

FAQ

Can a foreigner own 100% of a Polish LLC?

Yes. A foreign individual or foreign company may generally own 100% of the shares in a Polish LLC. Polish law does not generally require the shareholder to be resident in Poland. Immigration rules may become relevant only if the foreigner wants to live and manage the business from Poland.

How long does it take to register a Polish LLC?

Online registration through S24 usually takes around 2–5 business days if all signatures and documents are ready. Traditional notarial incorporation often takes longer, usually several weeks and sometimes 1–2 months. The timeline depends mainly on the availability of foreign documents, sworn translations and the workload of the registry court.

What is the minimum share capital of a Polish LLC?

The minimum share capital of a Polish LLC is PLN 5,000. The minimum nominal value of one share is PLN 50. The share capital may be higher if required by investors, banks, licensing rules or business credibility.

What taxes does a Polish LLC pay?

A Polish LLC usually pays corporate income tax, VAT if registered or required, withholding tax in some cross-border payments, and employment-related taxes if it hires staff. The standard CIT rate is 19%, while eligible small taxpayers may use the 9% rate. Some companies may choose Estonian CIT if they meet the conditions.

Do I need to be physically present in Poland to set up a Polish LLC?

Not always. A Polish LLC can often be incorporated remotely through a representative acting under a properly prepared power of attorney. Physical presence may be helpful or required in some banking, notarial or identity verification procedures, but it is not always necessary for incorporation itself.

How does Estonian CIT work in Poland?

Under Estonian CIT, a company generally does not pay current CIT on profits that remain in the company and are reinvested. Tax is typically paid when profits are distributed, for example as dividends. This model is often attractive for companies that plan to grow and reinvest rather than distribute profits every year.

Does a Polish LLC have to register for VAT?

Not every Polish LLC must register for VAT from the first day of activity. VAT registration is required or advisable depending on the type of business, expected turnover, cross-border transactions and counterparties’ expectations. Companies planning B2B trading, imports, exports or intra-EU transactions should analyse VAT registration before issuing their first invoice.

I hope this article clarified many things for you.

If not, please note that our experts will answer all your questions.

Get in touch with Intertax.