Personal Income Tax (PIT) in Poland – 2026 Complete Guide

What Is Personal Income Tax (PIT) in Poland?

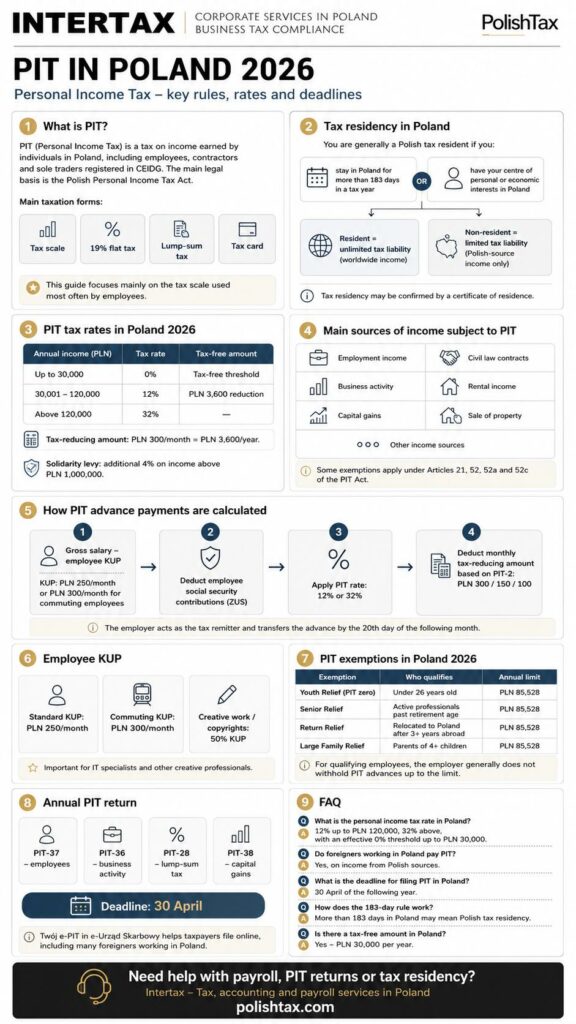

PIT, or Personal Income Tax in Poland, is a tax imposed on income earned by individuals, including employees, contractors and sole traders registered in CEIDG. The basic rules of PIT are regulated by the Polish Personal Income Tax Act — Ustawa o podatku dochodowym od osób fizycznych — which governs taxation of income earned by natural persons.

In Poland, income of individuals may be taxed under four main forms: progressive tax scale, 19% flat tax, lump-sum tax on registered revenue and tax card. For business income, the progressive tax scale is treated as the basic form of taxation, while the flat tax and lump-sum taxation generally require a specific choice by the taxpayer.

This article focuses mainly on the progressive tax scale, as it is the most common method of PIT taxation for employees in Poland and the default reference point for many individual taxpayers.

Who Is Subject to PIT in Poland? Tax Residency Rules

Tax residency in Poland determines whether an individual is subject to unlimited or limited tax liability in Poland. A person is generally treated as a Polish tax resident if they either spend more than 183 days in Poland in a tax year or have their centre of personal or economic interests — often called their centre of vital interests — in Poland.

A Polish tax resident is subject to unlimited tax liability in Poland, which means that Poland may tax their worldwide income, regardless of where it is earned. By contrast, a non-resident is subject only to limited tax liability in Poland, meaning that they are taxed in Poland only on income earned from Polish sources, unless an applicable double tax treaty provides otherwise. The Polish tax authorities also explain that non-residents generally settle in Poland only income earned in Poland.

Tax residency may be confirmed by a certificate of tax residence, which is an official document confirming the taxpayer’s place of residence or seat for tax purposes. The Polish tax residence certificate application refers to confirmation of residence in Poland for tax purposes and unlimited tax liability.

For a more detailed explanation, see our separate guide on Polish tax residency

PIT Tax Rates in Poland 2026

PIT tax rates in Poland in 2026 under the Polish income tax scale are 12% and 32%, with a tax-free amount of PLN 30,000. The 32% tax rate in Poland applies only to income exceeding PLN 120,000 per year, while income up to PLN 30,000 is effectively tax-free under the general rules of the tax scale. The Ministry of Finance confirms that, under the tax scale applicable from 2022, tax is calculated as 12% minus PLN 3,600 up to PLN 120,000, and PLN 10,800 plus 32% of the surplus above PLN 120,000 for higher income.

|

Annual Income (PLN) |

Tax Rate |

Tax-Free Amount |

|

Up to 30,000 PLN |

0% |

Tax-free threshold |

|

30,001 – 120,000 PLN |

12% |

PLN 3,600 reduction |

|

Above 120,000 PLN |

32% |

— |

The PLN 3,600 tax-reducing amount corresponds to the PLN 30,000 tax-free amount, because 12% of PLN 30,000 equals PLN 3,600. For employees, this reduction may be applied through monthly payroll calculations as PLN 300 per month, which gives PLN 3,600 annually.

High-income individuals should also consider the solidarity levy. This is an additional 4% levy on the surplus of income exceeding PLN 1,000,000 in a tax year. It is separate from the standard PIT scale and may apply to individuals whose qualifying income exceeds the statutory threshold.

Sources of Income Subject to PIT

The sources of income subject to PIT in Poland include employment income, civil law contracts, business activity, rental income, capital gains and income from the sale of property. Under Article 10 of the Polish Personal Income Tax Act, PIT applies to income earned by individuals from various statutory sources, unless a specific exemption or exclusion applies.

The main sources of income covered by PIT in Poland include:

|

Source of income |

Examples |

|

Employment and similar relationships |

employment contract, service relationship, cooperative employment, pensions |

|

Activities performed personally |

civil law contracts, management contracts, board remuneration, independent personal services |

|

Non-agricultural business activity |

sole proprietorship, B2B activity, professional services |

|

Special departments of agricultural production |

selected forms of agricultural production taxed under PIT rules |

|

Rental, lease and similar agreements |

private rental, lease of property or rights |

|

Capital gains and property rights |

dividends, interest, securities, shares, derivatives, copyrights and other property rights |

|

Sale of property and rights |

sale of real estate, cooperative ownership rights, perpetual usufruct rights or movable property, if taxable under PIT rules |

|

Other sources |

income not classified under the specific categories above |

However, not every amount received by an individual is automatically taxable. The PIT Act provides for numerous exemptions and special rules, including income listed in Articles 21, 52, 52a and 52c of the Polish Personal Income Tax Act, as well as cases where tax collection has been abandoned under separate tax regulations.

PIT should also be distinguished from other Polish taxes. For business transactions, VAT in Poland may apply separately to supplies of goods and services — see our guide to VAT in Poland. Companies and other corporate taxpayers may instead be subject to Corporate Income Tax — see our guide to CIT in Poland

How Is PIT Advance Payment Calculated in Poland?

A PIT advance payment in Poland is usually calculated and withheld by the employer during the year. In this arrangement, the employer acts as the tax remitter — often referred to in practice as a withholding taxpayer — while the employee remains the actual taxpayer responsible for personal income tax on employment income.

For employment income, the monthly PIT advance is generally calculated in the following steps:

-

Determine the taxable base

The starting point is the employee’s gross employment income. The employer deducts standard employee costs of earning income, usually PLN 250 per month or PLN 300 per month if the employee lives outside the locality where the workplace is located and does not receive a separation allowance or reimbursed commuting costs. The Ministry of Finance confirms annual equivalents of PLN 3,000 and PLN 3,600 respectively, which correspond to PLN 250 and PLN 300 per month. -

Deduct employee social security contributions

The taxable base is then reduced by the employee’s social security contributions financed from the employee’s own funds, such as pension, disability and sickness insurance contributions. -

Apply the PIT rate

The employer applies the Polish income tax scale: 12% up to the annual threshold of PLN 120,000 and 32% on income exceeding that threshold. -

Deduct the monthly tax-reducing amount

If the employee has submitted the relevant PIT-2 statement, the employer may reduce the monthly PIT advance by part of the annual tax-reducing amount. Depending on the employee’s declaration and the number of tax remitters using the reduction, this may be PLN 300, PLN 150 or PLN 100 per month. The official PIT-2 form allows the taxpayer to apply the tax-reducing amount as 1/12, 1/24 or 1/36 of the annual amount.

The employer transfers withheld PIT advances to the tax office generally by the 20th day of the month following the month in which the advance was collected. Correct payroll calculation is therefore important not only for the employee’s net salary, but also for the employer’s compliance as a tax remitter.

For support with monthly salary calculations, tax remitter obligations and employee PIT settlements, see our payroll services in Poland.

Costs of Earning Income (KUP) for Employees

Koszty uzyskania przychodu for employees in Poland are standard monthly tax-deductible costs applied when calculating PIT on employment income. The basic KUP deduction is PLN 250 per month for employees who live in the same locality as their workplace. Increased costs of PLN 300 per month may apply to commuting employees who live outside the locality where the workplace is located, provided the statutory conditions are met.

For employees performing creative work, Polish PIT rules may allow 50% tax-deductible costs for income related to the use or transfer of copyrights or related rights. The Ministry of Finance explains that these costs apply to creative work involving copyrights or related rights and are calculated on revenue reduced by social security contributions withheld by the payer in a given month.

This rule can be particularly important for employers hiring IT specialists, software developers, designers, engineers and other creative professionals, where part of the remuneration may relate to copyrighted works. In practice, applying 50% KUP requires proper employment documentation, separation of creative remuneration and evidence that copyright-protected work is actually created and transferred or used.

PIT Exemptions in Poland 2026: Who Doesn’t Pay?

PIT exemptions in Poland in 2026 may allow certain individuals to earn income without paying personal income tax up to an annual limit of PLN 85,528. The most important exemptions include youth tax relief in Poland, often called PIT zero for young people, as well as reliefs for working seniors, returning residents and parents of at least four children. The Polish Ministry of Finance confirms that the maximum annual exemption limit for these reliefs is PLN 85,528, even if a taxpayer meets the conditions for more than one relief.

|

Exemption |

Who Qualifies |

Annual Limit |

|

Youth Relief — zerowy PIT |

Individuals under 26 years old earning qualifying income, including employment income and certain civil law contract income |

PLN 85,528 |

|

Senior Relief |

Active professionals past retirement age who continue working and do not receive a pension covered by the statutory exclusion rules |

PLN 85,528 |

|

Return Relief |

Individuals who relocated their tax residence to Poland after living abroad for at least 3 years, subject to statutory conditions |

PLN 85,528 |

|

Large Family Relief |

Parents or guardians raising at least 4 children, subject to statutory conditions |

PLN 85,528 |

For employees who qualify for one of these exemptions, the relief usually means that the employer does not withhold PIT advances on qualifying employment income up to the applicable limit. In other words, if the employee provides the required statement and meets the statutory conditions, the employer should not deduct Polish PIT from the covered part of the salary during payroll calculation.

These exemptions do not always apply to every type of income. For example, the youth relief applies only to specific categories of income, and the Ministry of Finance notes that it does not cover management contracts or similar contracts. Therefore, each exemption should be checked against the employee’s age, residence status, family situation, type of income and documents submitted to the employer.

Key Tax Reliefs When Filing Annual PIT Return

PIT reliefs in Poland may reduce the final annual tax due or the taxable income reported in the annual PIT return. The most common reliefs include child tax relief, rehabilitation relief, internet relief, IKZE pension savings relief and thermomodernisation relief. Some taxpayers may also benefit from joint tax filing with a spouse, which can be particularly advantageous when one spouse has significantly lower income.

|

Tax relief |

Short description |

|

Child tax relief — child tax relief Poland |

A deduction from tax for parents, legal guardians or foster families raising children. The annual amount is PLN 1,112.04 for the first child, PLN 1,112.04 for the second child, PLN 2,000.04 for the third child and PLN 2,700.00 for the fourth and each subsequent child. |

|

Rehabilitation relief |

Available to disabled persons or taxpayers supporting disabled persons, for selected rehabilitation expenses and expenses facilitating everyday life. |

|

Internet relief |

Allows deduction of actual expenses for internet use, up to PLN 760 per taxpayer, generally only for two consecutive tax years. |

|

IKZE relief |

Allows deduction of payments made to an Individual Retirement Security Account — IKZE — within the statutory annual limit. The deduction is made in the annual return, not when calculating monthly tax advances. |

|

Thermomodernisation relief |

Available to owners or co-owners of single-family residential buildings who incur qualifying thermomodernisation expenses. The deduction is limited to PLN 53,000 per taxpayer. |

Joint tax filing with a spouse

Joint tax filing by spouses in Poland may be available if the spouses were married and had matrimonial property community for the relevant period required by law. It is also possible for spouses who married during the tax year, provided they remained married and in matrimonial property community until the last day of that year.

The main benefit of joint filing is that the tax is calculated on half of the spouses’ combined taxable income and then doubled. This may reduce the total PIT burden, especially where one spouse has no income, low income or income below the second tax threshold, while the other spouse earns more.

These reliefs and preferences are subject to detailed statutory conditions, documentation requirements and income limits. Each of them can justify a separate article, so in this PIT guide they should be treated as a practical overview rather than a full technical explanation.

What Income Is NOT Taxed? Key PIT Exemptions

PIT exempt income in Poland includes certain types of income that are excluded from taxation or covered by specific exemptions under the Polish Personal Income Tax Act. In practice, some of the most common examples of tax-free income in Poland relate to private sale of assets, statutory exemptions listed in Article 21 of the PIT Act and selected special-purpose reliefs.

Key examples include:

|

Type of income |

When it may be tax-free |

|

Sale of real estate |

Income from the private sale of real estate is generally not taxed if the sale takes place after 5 years, counted from the end of the calendar year in which the property was acquired or built. If the sale is made before that period, PIT may apply and the taxpayer may need to file PIT-39. |

|

Sale of movable property |

Private sale of movable property, such as a car or equipment, is generally not taxed if the sale takes place after 6 months, counted from the end of the month in which the item was acquired. |

|

Selected statutory exemptions under Article 21 |

Article 21 of the PIT Act contains a broad catalogue of exempt income, including selected damages, benefits, allowances, scholarships, social assistance benefits and other payments meeting statutory conditions. |

|

Reliefs for selected taxpayers |

Some income may also be exempt under special PIT reliefs, such as youth relief, return relief, senior relief or large family relief, subject to annual limits and detailed statutory requirements. |

These exemptions should be checked carefully because the PIT treatment often depends on the type of income, timing, documentation and whether the transaction is private or business-related. This section is only a practical overview — a full analysis of Article 21 exemptions and special PIT reliefs should be covered in separate, dedicated articles.

Penalties for Failing to Pay PIT Advance Payments

-

PIT penalties in Poland may apply if an employer or another tax remitter fails to calculate, collect or transfer PIT advance payments on time. For employment income, the employer acts as the tax remitter and is legally responsible for withholding PIT advances from employees’ remuneration and transferring them to the competent tax office, generally by the 20th day of the following month.

-

Under the Polish Tax Ordinance, a tax remitter may be held liable for tax that was not collected or was collected but not paid to the tax office. If the tax authority identifies such failure, it may issue a decision determining the remitter’s liability for the unpaid amount.

-

In addition to tax liability, failure to pay collected tax may also result in fiscal criminal liability. Under Article 77 of the Polish Fiscal Penal Code, a tax remitter who does not transfer collected tax on time may face a fine of up to 720 daily rates, imprisonment for up to 3 years, or both penalties jointly.

-

Timely PIT settlements are therefore not only an accounting matter, but a legal obligation of the employer as a withholding tax remitter. To reduce compliance risk, employers should ensure that payroll, PIT advances and tax remitter obligations are handled correctly each month.

-

For professional support with PIT settlements, payroll compliance and tax remitter obligations in Poland, contact Intertax or see our tax services in Poland.

How to File an Annual PIT Return in Poland

To file a PIT return in Poland, taxpayers usually submit an annual tax return by 30 April of the year following the tax year. Employees most commonly file PIT-37, which is also pre-filled by the Polish tax administration in the Twój e-PIT service available through e-Urząd Skarbowy. The Ministry of Finance confirms that PIT returns for the previous year are made available in Twój e-PIT from 15 February, and the annual tax return deadline is 30 April.

The main annual PIT forms in Poland are:

PIT form |

Who uses it |

PIT-37 |

Employees, contractors and other individuals whose income was settled through a Polish tax remitter, such as an employer |

PIT-36 |

Individuals who must calculate tax independently, including many sole traders taxed under the general tax scale |

PIT-28 |

Taxpayers using lump-sum taxation on registered revenue, including selected entrepreneurs and private rental taxpayers |

PIT-38 |

Individuals reporting capital gains, such as income from the sale of securities or financial instruments |

The Twój e-PIT service simplifies annual filing because the tax office prepares selected returns using information received from employers, tax remitters and other institutions. In the service, taxpayers can review the pre-filled return, add reliefs and deductions, change the public benefit organisation for the 1.5% tax donation, accept the return or submit corrections.

For employees, PIT-37 and for investors PIT-38 may be automatically accepted after 30 April if the taxpayer does not submit or reject the return earlier. However, PIT-28, PIT-36 and PIT-36L are not automatically accepted and must be completed and approved by the taxpayer.

For foreigners living or working in Poland, e-Urząd Skarbowyand Twój e-PIT can be a practical way to access a pre-filled annual return online, verify income reported by Polish employers and submit the PIT return without visiting the tax office in person.

FAQ: Personal Income Tax in Poland

What is the personal income tax rate in Poland?

The personal income tax rate in Poland under the general tax scale is 12% up to PLN 120,000 of annual taxable income and 32% on income above PLN 120,000. There is also an effective 0% tax threshold up to PLN 30,000, because the annual tax-reducing amount corresponds to the tax-free amount.

Do foreigners working in Poland pay PIT?

Yes. Foreigners working in Poland generally pay PIT on income earned from Polish sources, regardless of whether they are Polish tax residents or non-residents. A Polish tax resident is taxed in Poland on worldwide income, while a non-resident is taxed only on Polish-source income, subject to applicable double tax treaties.

What is the deadline for filing PIT in Poland?

The standard deadline for filing an annual PIT return in Poland is 30 April of the year following the tax year. For many employees, the annual return is pre-filled by the tax administration in the Twój e-PIT system, available through e-Urząd Skarbowy.

How does the 183-day rule work in Poland?

Under the 183-day rule in Poland, a person who stays in Poland for more than 183 days in a tax year may be treated as a Polish tax resident. Polish tax residency means unlimited tax liability in Poland, so Poland may tax the individual’s worldwide income, unless a double tax treaty provides otherwise.

Is there a tax-free amount in Poland?

Yes. Poland has an annual tax-free amount of PLN 30,000 under the general PIT scale. This means that income up to PLN 30,000 is effectively not taxed under the tax scale, while income above that amount is taxed according to the 12% and 32% rates.

For a full breakdown of employer costs including ZUS contributions, see our guide The True Cost of Hiring an Employee in Poland

If you need support with PIT advance payments, our Payroll Team can help.