Polish Tax Residency. Rules, 183-Day Test & Certificate Guide (2026)

Polish tax residency determines whether you are taxed in Poland on your worldwide income or only on income earned from Polish sources. This distinction is crucial for returning Polish expats, foreigners working in Poland, digital nomads, and owners of foreign companies who manage or conduct business while physically present in Poland.

Executive Summary

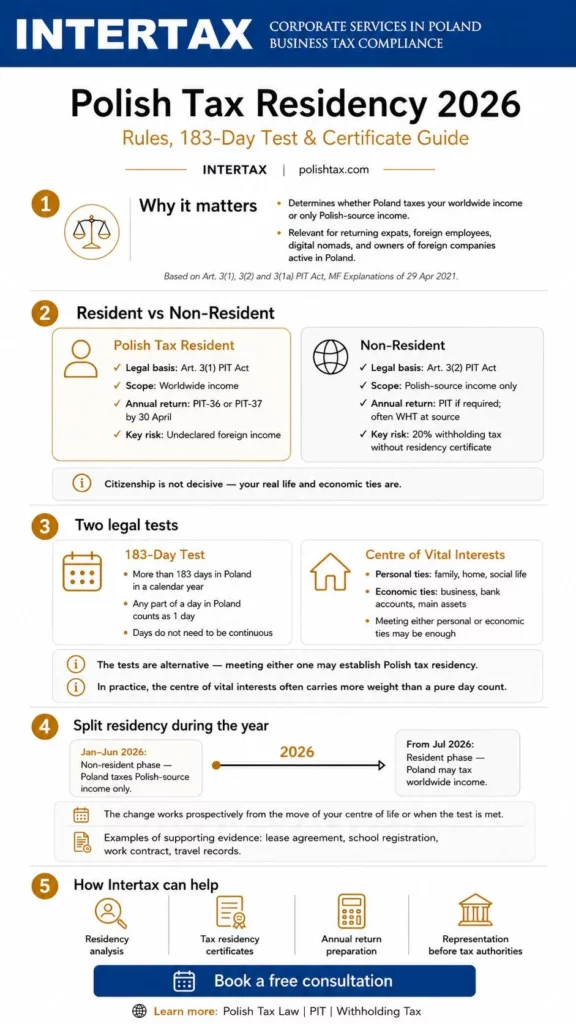

The following article explains in detail the rules for determining Polish tax residence, which determines whether a person is subject to unlimited tax liability (tax on total income) or limited tax liability (only on income earned in Poland) in Poland. Possession of Polish citizenship is not a decisive factor for residency. According to Polish regulations, the status of tax resident depends on meeting at least one of two alternative criteria: 183 days test: staying in Polish territory for more than 183 days in a tax year. This limit includes each day (or part thereof) of physical presence, including arrival days, departure days, weekends and holidays. The stay does not have to be continuous. Centre of personal or economic interests: having a main centre of private (e.g. family, social life, home) or economic (e.g. workplace, business, main assets, bank accounts) in Poland In the event that two countries recognize the same person as their resident, the conflict-of-law rules contained in double taxation treaties apply. The hierarchy of these rules includes: permanent residence, center of vital interests.

What Is Polish Tax Residency and What Does It Mean for You?

Polish tax residency determines the scope of your personal income tax obligations in Poland. In simple terms, Poland distinguishes between two types of tax liability: unlimited tax liability for Polish tax residents and limited tax liability for non-residents.

A Polish tax resident is generally required to report and settle tax in Poland on their worldwide income, regardless of whether that income was earned in Poland or abroad. This is known as unlimited tax liability and is based on Article 3(1) of the Polish PIT Act. By contrast, a non-resident is taxed in Poland only on income derived from Polish sources, such as Polish employment, Polish business activity, Polish real estate, or certain payments from Polish entities. This is known as limited tax liability under Article 3(2a) of the PIT Act.

Importantly, Polish citizenship is not the deciding factor. A Polish passport alone does not make someone a Polish tax resident, and a foreign passport does not prevent Polish tax residency. What matters is where the person actually lives, works, maintains their personal and economic ties, and whether Poland is their centre of personal or economic interests.

| Polish Tax Resident | Non-Resident | |

| Legal basis | Art. 3(1) PIT Act | Art. 3(2a) PIT Act |

| Scope | Worldwide income | Polish-source income only |

| Annual return | Usually PIT-36 or PIT-37, by 30 April | PIT return if required; often tax withheld at source |

| Key risk | Undeclared foreign income | 20% withholding tax without a valid tax residency certificate |

Two Legal Criteria for Polish Tax Residency under Article 3(1a) of the PIT Act

Under Article 3(1a) of the Polish PIT Act, an individual is treated as having their place of residence for tax purposes in Poland if at least one of the following two conditions is met:

- they have their centre of personal or economic interests in Poland, often referred to as the “centre of vital interests”; or

- they stay in Poland for more than 183 days in a tax year.

These criteria are alternative, not cumulative. This means that a person does not need to meet both tests at the same time. Spending fewer than 183 days in Poland does not automatically exclude Polish tax residency if the person’s personal or economic life is centred in Poland. Likewise, a stay exceeding 183 days may trigger Polish tax residency even where some personal or business ties remain abroad.

In practice, the centre of life test is usually more important than the mechanical day-count test. Polish tax authorities and administrative courts look beyond the number of days spent in Poland and examine where the person’s real personal and economic connections are located. This approach was confirmed by the Supreme Administrative Court in its judgment of 28 September 2018, case no. II FSK 2653/16, where the court emphasised that determining tax residence requires an overall assessment of the taxpayer’s life circumstances, not a purely formal or arithmetic analysis.

Criterion 1: 183 Days of Physical Presence in Poland

The first statutory criterion concerns the length of an individual’s physical presence in Poland. Under Article 3(1a) of the Polish PIT Act, a person may be treated as a Polish tax resident if they stay in Poland for more than 183 days in a tax year.

For this purpose, the physical presence method is used. This means that any part of a day spent in Poland is generally counted as one full day. Arrival days, departure days, weekends, holidays and short visits may therefore all be relevant when calculating the total number of days spent in Poland.

The stay does not have to be continuous. What matters is the total number of days of physical presence in Poland during the calendar year, not a single uninterrupted period of residence. Several shorter visits may therefore add up to more than 183 days.

This approach is consistent with the Polish Ministry of Finance’s Tax Explanations of 29 April 2021 on tax residency and the scope of tax liability of individuals in Poland, issued under Article 14a § 1 point 2 of the Polish Tax Ordinance. The explanations confirm that the 183-day test is one of the statutory residency criteria, alongside the centre of personal or economic interests test.

However, exceeding 183 days in Poland should not be treated mechanically. In practice, the 183-day test must be analysed together with the taxpayer’s centre of vital interests. If the facts clearly show that the individual’s personal and economic life is centred in another country, the final residency position may require a broader analysis, including the relevant double tax treaty and its tie-breaker rules. This is why the centre of vital interests test often has practical priority over a purely numerical day count.

Criterion 2: Centre of Vital Interests: Personal or Economic

The second criterion is the centre of vital interests, which refers to the place where an individual’s main personal or economic ties are located. Under Article 3(1a) of the Polish PIT Act, it is enough for a person to have either their centre of personal interests or their centre of economic interests in Poland. These are alternative sub-criteria, so both do not have to be met at the same time.

The centre of personal interests usually includes the individual’s closest private and social connections. In practice, Polish tax authorities and courts may look at where the taxpayer’s spouse, partner or children live, where they maintain a home, where they participate in social life, and whether they belong to Polish professional, cultural, sports or community organisations.

The centre of economic interests focuses on the taxpayer’s financial and business links. Relevant factors may include the place where the person runs or manages a business, where their main professional activity is performed, where they hold bank accounts, where their key assets are located, and where they derive most of their income.

A useful example is the judgment of the Provincial Administrative Court in Kraków of 10 August 2023, case no. I SA/Kr 579/23. The court considered that a taxpayer could still have their centre of personal interests in Poland even when staying abroad for a significant period, because the taxpayer’s family and personal ties remained in Poland and the foreign stay was temporary or exceptional. The case confirms that tax residency is assessed on the basis of real-life connections, not only the number of days spent in a given country.

Split Tax Residency: Changing Residency During the Tax Year

Polish tax residency does not always have to apply for the entire calendar year. In some cases, a person may change their tax residence during the year. This is often referred to as split tax residency.

According to the Polish Ministry of Finance’s Tax Explanations of 29 April 2021, tax residence should be assessed by reference to the taxpayer’s actual personal and economic circumstances. As a result, a move to or from Poland may change the scope of Polish tax liability during the same tax year, especially where the taxpayer transfers their centre of vital interests or meets the statutory day-count criterion.

The change generally works prospectively, not retroactively. This means that Polish unlimited tax liability should apply from the date on which the individual becomes Polish tax resident, for example from the day they move their centre of personal or economic interests to Poland, or from the point at which the relevant residency conditions are met. Before that date, the person may remain subject only to limited tax liability in Poland, unless a double tax treaty provides otherwise.

Example:

A Polish expat has lived and worked in Germany for several years. In July 2026, they return to Poland with their spouse and children, rent or buy a home in Poland, enrol their children in a Polish school, move their main bank accounts and begin working from Poland. In this case, the first half of 2026 may still fall under non-resident treatment in Poland, meaning that Poland taxes only Polish-source income, if any. From the date of the move in July 2026, the taxpayer may become a Polish tax resident and may be required to report worldwide income in Poland for the second half of the year.

This split should be reflected in the annual Polish tax return. Depending on the type of income, the taxpayer may need to file PIT-36 and disclose foreign income for the Polish-resident part of the year. Where foreign income is reported, the taxpayer may also need to attach PIT/ZG, which is used to show income earned abroad and the relevant method of avoiding double taxation.

In a split-residency case, documentation is essential. The taxpayer should keep evidence showing the exact timing and substance of the move, such as:

| Evidence | Why it matters |

| Lease agreement or property purchase documents in Poland | Shows when a permanent home became available in Poland |

| Termination of foreign lease or sale of foreign home | Supports the relocation of the taxpayer’s household |

| School or kindergarten registration for children | Demonstrates transfer of family and personal life to Poland |

| Employment contract, business registration or board resolutions | Shows where work, business or management activity is actually performed |

| Bank account records and asset transfers | Helps evidence the location of economic interests |

| Travel records, boarding passes and calendar entries | Supports the physical presence analysis |

| Utility bills, insurance policies and local registrations | Confirms real day-to-day residence in Poland |

Split residency is therefore not just a formal declaration. It should be supported by a coherent factual record showing when the taxpayer’s centre of vital interests moved to Poland and how income should be allocated between the non-resident and resident parts of the year.

What If Two Countries Claim You as a Tax Resident? Tie-Breaker Rules

Dual tax residency may occur when two countries treat the same individual as their tax resident under their domestic rules. For example, Poland may claim residency because the person’s family or business interests are in Poland, while another country may claim residency because the person spends significant time there or holds a permanent home there.

In such cases, the conflict is usually resolved under the relevant double tax treaty. Most Polish double tax treaties follow the structure of Article 4 of the OECD Model Tax Convention, which contains a sequence of “tie-breaker” rules for individuals. These rules are applied step by step, until one treaty residence is determined. The OECD describes the Model Convention as a framework for resolving common problems of international juridical double taxation.

The usual hierarchy is as follows:

| Step | Tie-breaker rule | Practical meaning |

| 1 | Permanent home | In which country does the individual have a permanent home available for their use? |

| 2 | Centre of vital interests | If a permanent home exists in both countries, where are the person’s closer personal and economic relations? |

| 3 | Habitual abode | If the centre of vital interests cannot be determined, in which country does the person stay more regularly? |

| 4 | Nationality | If habitual abode does not resolve the issue, which country is the person a national of? |

| 5 | Mutual Agreement Procedure, MAP | If the conflict still remains, the competent tax authorities should resolve it by mutual agreement. |

For Polish purposes, double tax treaties are particularly important because they may override domestic tax rules. Under Article 91 of the Constitution of the Republic of Poland, a ratified international agreement forms part of the Polish legal order and, if ratified with prior statutory consent, has precedence over statutes where the two cannot be reconciled.

From a practical perspective, anyone facing a possible dual-residency situation should consider obtaining a tax residency certificate from the other country before Polish tax obligations arise. A foreign certificate does not automatically defeat Polish tax residency, but it is often a key document when applying a treaty, avoiding excessive withholding tax, supporting a payroll position, or preparing evidence for a future tax audit.

Polish Tax Residency Certificate: How and Where to Obtain It

A Polish tax residency certificate is an official document confirming that a person or entity has their place of residence or registered seat in Poland for tax purposes. In practice, it is used to prove Polish tax residence to foreign tax authorities, foreign payers, banks, platforms, or business counterparties applying double tax treaty benefits.

The application is filed on form CFR-1: “Application for a certificate of residence or registered seat for tax purposes in Poland.” The form may be used by individuals as well as companies and other entities requesting confirmation of Polish tax residence. The official CFR-1 form refers to confirmation of residence or seat in Poland for tax purposes and Polish unlimited tax liability under the relevant treaty.

The application may generally be submitted:

| Method | Practical note |

| Tax office | Paper application filed with the competent Polish tax office |

| e-Urząd Skarbowy | Online submission through the Polish e-Tax Office |

| ePUAP | Electronic filing using a trusted profile or qualified signature |

The certificate should be issued within 7 days from filing the application, provided the applicant is entitled to receive it and the application is complete. Some tax office guidance also indicates that the certificate is released to the authorised person after identity verification.

A Polish certificate may be issued either for a specified period or without a fixed end date, depending on the wording of the request and the taxpayer’s situation. The CFR-1 form allows the applicant to request that the “valid until” field not be completed where, as at the date of issuing the certificate, the applicant resides or has their seat in Poland for tax purposes.

For companies, tax residency certificates are especially important in withholding tax transactions. Where payments such as dividends, interest, royalties or certain intangible services are made cross-border, a Polish payer usually needs a valid certificate of the foreign recipient’s tax residence before applying a treaty rate or exemption. For related-party passive payments exceeding PLN 2 million per year per taxpayer, Poland may apply the “pay and refund” mechanism, under which WHT is collected at the statutory rate on the excess and a refund must be claimed later, unless an available exception applies.

Tax Obligations After Establishing Polish Tax Residency

Once you become a Polish tax resident, your Polish tax obligations expand significantly. In most cases, you are required to report not only Polish income, but also income earned abroad, including employment income, business income, rental income, dividends, interest, capital gains, pensions, and other taxable foreign-source income.

A Polish tax resident generally files an annual personal income tax return, usually PIT-36 or PIT-37, by 30 April of the year following the tax year. PIT-36 is commonly used where the taxpayer has foreign income, business income, or income that must be self-assessed, while PIT-37 is typically used for income settled through Polish remitters, such as employers. The official Polish tax portal confirms that PIT-36 and PIT-37 are among the annual returns filed between 15 February and 30 April of the following year.

Foreign income does not always mean double taxation in practice. Poland applies the relevant double tax treaty or, where no treaty applies, domestic rules for avoiding double taxation. The two main methods are:

| Method | How it works in practice |

| Exemption with progression | Foreign income is exempt from Polish tax, but it may increase the tax rate applied to Polish taxable income. |

| Proportional tax credit | Foreign income is taxed in Poland, but foreign tax paid may be credited against Polish tax, subject to statutory limits. |

The applicable method depends on the relevant double tax treaty and may be affected by the MLI, which has changed the method of avoiding double taxation in many Polish treaties to the tax credit method.

Where foreign income is reported, the taxpayer may also need to file PIT/ZG as an attachment to the annual return. PIT/ZG is used to disclose income earned abroad and the method used to avoid double taxation.

Tax residents should also review whether they have any reporting obligations connected with foreign assets, rights, bank accounts, shares or interests in foreign entities. In particular, form ORD-HZ may be relevant where the tax authority requires a taxpayer to disclose real estate, property rights, movable assets or transferable property rights that may secure tax liabilities. It should not be treated as a routine annual attachment for every Polish tax resident, but it may become important in tax proceedings, audits or enforcement-related situations.

Another issue to consider is exit tax. Although exit tax is mainly relevant when a person leaves Poland or transfers assets out of the Polish tax jurisdiction, it should be reviewed when a taxpayer has significant shares, securities, business assets or foreign structures. In broad terms, Polish exit tax concerns taxation of unrealised gains in certain situations where Poland loses the right to tax future disposal gains.

A practical compliance review after becoming Polish tax resident should therefore include:

| Area | What to check |

| Annual PIT return | Whether PIT-36 or PIT-37 is required and whether all foreign income is included |

| PIT/ZG | Whether foreign income must be disclosed by country and income type |

| Foreign tax paid | Whether the exemption with progression or proportional credit method applies |

| Foreign accounts and assets | Whether any disclosure is required, especially if requested by the tax authority |

| Foreign companies or shares | Whether additional Polish reporting, CFC or beneficial-owner analysis is needed |

| Exit tax exposure | Whether assets or residency changes could trigger taxation of unrealised gains |

If a taxpayer discovers that foreign income was omitted from a Polish return, it is usually advisable to act before the tax authority identifies the issue. Depending on the circumstances, the taxpayer may file a corrected tax return and, where appropriate, submit a voluntary disclosure known as czynny żal. This may help reduce the risk of fiscal penal liability, provided it is filed effectively and before the authority has documented knowledge of the offence.

FAQ – Polish Tax Residency: Most Common Questions

Can I be a Polish tax resident if I spend less than 183 days in Poland?

Yes. The 183-day test is only one of the two alternative criteria for Polish tax residency. You may still be treated as a Polish tax resident if your centre of personal or economic interests is in Poland, even if you spend fewer than 183 days in Poland during the tax year.

What exactly counts as “centre of vital interests” in Poland?

The centre of vital interests means the place where your main personal or economic connections are located. Personal ties may include your spouse, partner, children, home, social life, or membership in organisations. Economic ties may include your business, employment, bank accounts, key assets, investments, or the place where you manage your financial affairs.

Does Polish citizenship determine tax residency?

No. Polish citizenship does not determine tax residency. A Polish citizen living permanently abroad may be a non-resident in Poland, while a foreign citizen living and working in Poland may become a Polish tax resident. The decisive factors are where you actually live, where your personal and economic interests are located, and how much time you spend in Poland.

How do I obtain a Polish tax residency certificate?

You can apply for a Polish tax residency certificate by filing form CFR-1 with the competent Polish tax office. The application may usually be submitted in paper form, through e-Urząd Skarbowy, or via ePUAP. The certificate should generally be issued within 7 days, provided the application is complete and the tax office confirms that you are resident in Poland for tax purposes.

What happens if I am considered a tax resident in two countries at the same time?

If two countries claim you as a tax resident, the conflict is usually resolved under the relevant double tax treaty. Most treaties apply tie-breaker rules in the following order: permanent home, centre of vital interests, habitual abode, nationality, and finally mutual agreement between tax authorities. The treaty result may override domestic Polish rules.

Can I change my tax residency in the middle of the year?

Yes. Polish tax residency may change during the tax year if your factual circumstances change. For example, if you move your family, home, work, and main economic interests to Poland in July, you may be treated as a non-resident for the first part of the year and as a Polish tax resident from the date of the move. This split should be properly reflected in your annual tax return, especially where foreign income is involved.

How Intertax Can Help

Polish tax residency is highly fact-specific. A small change in where you live, work, manage your business, keep your assets, or spend time with your family may affect whether Poland can tax your worldwide income. Intertax helps individuals, entrepreneurs, remote workers, expats and foreign business owners assess their Polish tax residency position and manage the related compliance risks.

Our support may include:

Tax residency analysis – Review of your personal and economic ties, 183-day presence, treaty position and risk of dual residency.

Tax residency certificates – Assistance with obtaining Polish tax residency certificates and reviewing foreign certificates for Polish tax purposes.

Annual Polish tax returns – Preparation or review of PIT-36, PIT-37, PIT/ZG and foreign-income disclosures.

Double taxation issues – Analysis of the applicable double tax treaty and the correct method for avoiding double taxation.

Withholding tax matters – Support with tax residency documentation, WHT relief, treaty rates and pay-and-refund procedures.

Representation before tax authorities – Assistance in correspondence, audits, explanations, voluntary disclosures and disputes with Polish tax offices.

Intertax provides Polish Tax Consultancy and compliance support for businesses and individuals, including CIT and PIT compliance, Withholding Tax issues and representation in dealings with the Polish tax administration.