Why Invest in Poland? Strategic Advantages for Foreign Businesses (2026 Guide)

Executive Summary

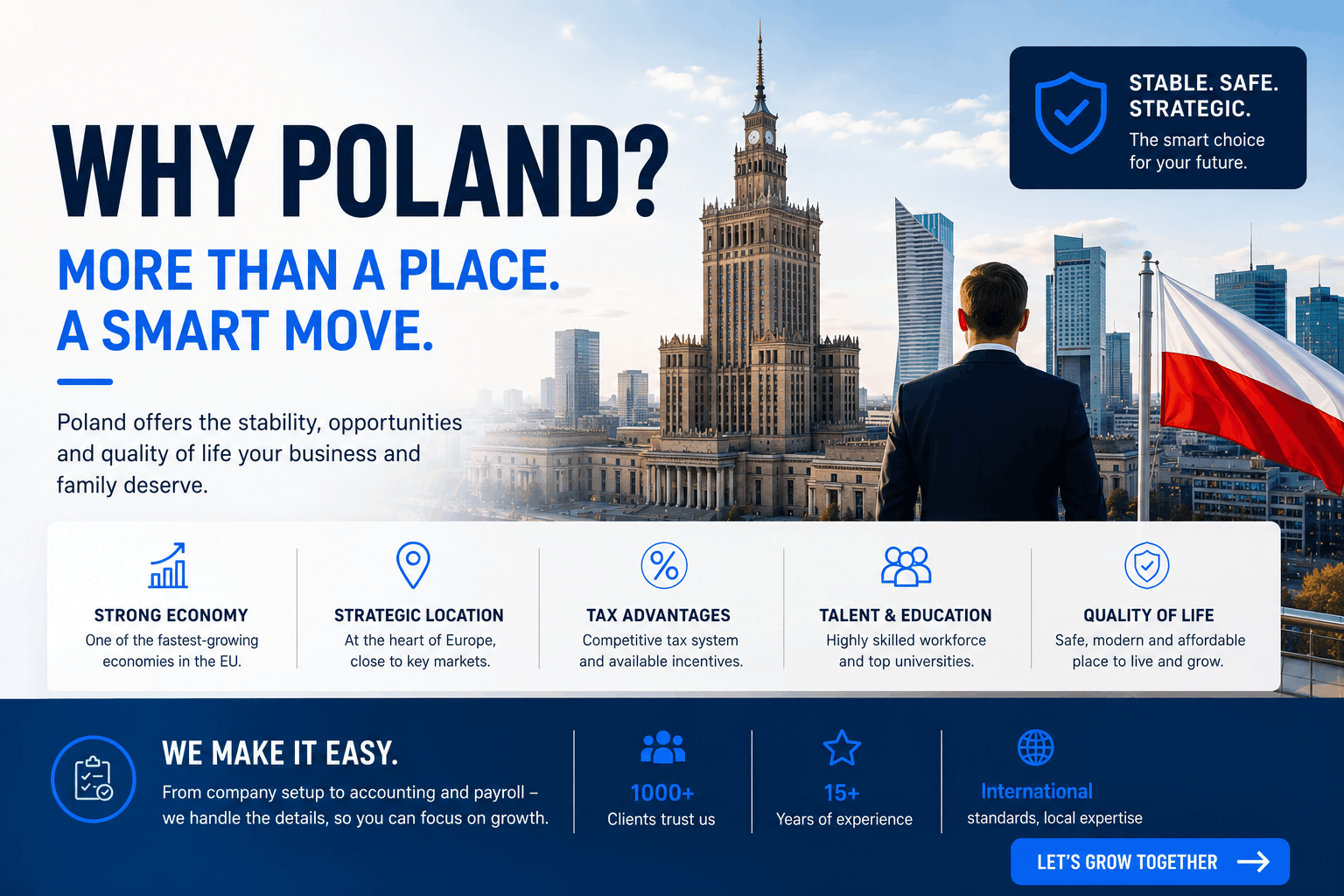

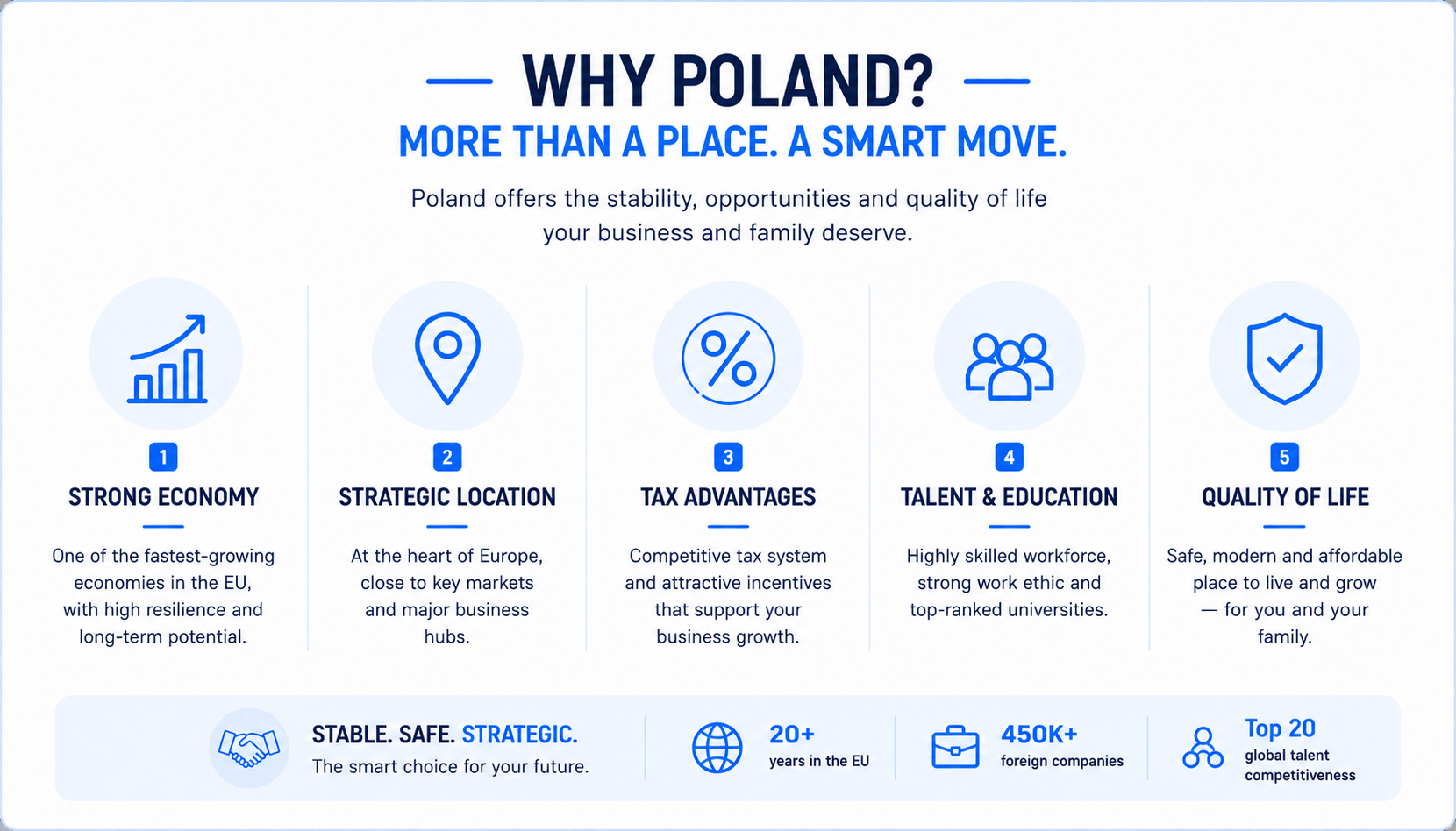

Poland is one of the most commercially attractive EU entry points for foreign investors that need three things at once: access to the European market, a large and skilled workforce, and tax or investment mechanisms that can improve project economics. For many foreign companies, the decision is not whether Poland looks promising in theory. It is whether Poland can support a faster, safer and more tax-efficient expansion than the alternatives. In many cases, the answer is yes, especially when the entry model is structured correctly from the start.

Who this guide is for

This guide is written for CFOs, founders, in-house counsel, finance leaders and expansion managers who are comparing Poland with other European locations. If your team is weighing tax efficiency, labour availability, compliance burden, market access and implementation speed, the sections below are meant to help you make that decision with less guesswork.

Book a free initial consultation if you want to assess your specific expansion model before choosing a structure, registering for VAT, or setting up payroll.

For foreign businesses evaluating expansion into Central Europe, Poland stands out less as a low-cost story and more as a strategic operating platform. The country offers access to the EU single market, a sizeable domestic economy, a strong industrial and services base, and an incentive framework that can materially improve project economics. OECD projections published for Poland point to real GDP growth of 3.4% in 2025 and 3.0% in 2026, while public and official materials continue to show Poland as a major destination for regional investment projects.

If you are deciding where to establish an entity, warehouse, shared-services centre, or long-term operational hub, the real question is not simply “why Poland?” It is whether Poland gives your business a better mix of speed, cost control, growth potential and compliance predictability than the alternatives. In many expansion models, it does.

Why Poland Can Be the Right Entry Point

Poland is usually a strong choice when a foreign investor needs a location that can support both execution and scale. That can mean manufacturing with EU distribution, a finance or operations centre serving several jurisdictions, a logistics base close to Germany and the wider CEE region, or a technology team with enough labour depth to keep hiring after launch.

- You need an EU base with room to scale beyond one city.

- You want to combine tax efficiency with operational substance, not paper structuring alone.

- You need access to multilingual talent across finance, payroll, IT, operations or compliance.

- You want a location that can serve both Poland itself and the wider CEE market.

- You need support with VAT, entity setup, payroll, fiscal representation or KSeF readiness during entry.

1. Strategic Location at the Heart of Europe

Poland sits between Western Europe and the wider CEE region, bordering seven countries and giving investors direct overland access to Germany, Czechia, Slovakia, Lithuania, Ukraine, Belarus, and Russia’s Kaliningrad region. For many supply chains, that means one location can serve both the EU core and fast-moving regional distribution routes.

Infrastructure has improved substantially over the last decade. Poland’s expressway and motorway network exceeded 4,900 km in official road authority reporting, and further expansion is ongoing. The country also benefits from an extensive rail network, major Baltic seaports, and airport capacity that supports both passenger mobility and freight. For investors thinking beyond today’s network, the Centralny Port Komunikacyjny project remains relevant as a long-term transport and high-speed rail upgrade with clear implications for logistics and business mobility.

In commercial terms, this matters because transport, distribution and management oversight become easier to coordinate from one location. Poland is close enough to Western Europe for tightly managed supply chains, but large enough to justify local production, service delivery, and back-office investment in its own right.

2. Competitive Tax System and Investment Incentives

For many investors, this is the decisive section. Poland’s tax system is not the simplest in Europe, but it can be commercially attractive when the structure matches the business model. Standard CIT is 19%, and eligible smaller taxpayers can use 9% on qualifying income where revenue thresholds and status conditions are met. The bigger opportunity, however, often lies in how headline tax interacts with investment incentives, profit-retention strategy, IP treatment and cross-border structuring.

The Polish Investment Zone is one of the most important tools available to new investors. Since 2018, the system has operated on a nationwide basis rather than being limited to classic special economic zone plots. In practice, this means that an investor may obtain income tax relief linked to a new investment, with regional aid intensity potentially reaching up to 70% of eligible costs in some locations and investor profiles. The final outcome depends on the region, company size and project details, so this benefit should be modelled rather than assumed. When it is handled early, though, it can materially improve project economics.

Estonian CIT can also be powerful for companies that intend to reinvest profits rather than distribute them immediately. Instead of applying classical current taxation in the same way as standard CIT, the model generally defers tax until profit distribution or a comparable event. For expanding businesses, that can support internal financing, reduce short-term cash pressure and improve timing efficiency.

Innovation-led businesses should also review IP Box. Poland allows a preferential 5% rate on qualifying IP income, which may be relevant for software, R&D and technology-led operations if the underlying documentation and nexus requirements are managed correctly. In some cases, holding-company or participation-type exemptions may also improve the tax profile of dividend or share-disposal flows, although those rules should be reviewed case by case rather than treated as automatic.

Poland’s double tax treaty network remains another strategic advantage. The Ministry of Finance’s public treaty register lists more than 90 treaties, which can help with cross-border withholding tax planning, profit repatriation and broader international structuring.

| Tax instrument | Rate / benefit | Best fit |

|---|---|---|

| Standard CIT | 19% | Most corporate taxpayers |

| Small business CIT | 9% | Eligible smaller taxpayers meeting revenue and status tests |

| Polish Investment Zone | Income tax relief linked to eligible new investment; in some cases up to 70% of eligible costs | Manufacturing, logistics, service and expansion projects |

| Estonian CIT | Tax deferred until profit distribution or equivalent event | Companies reinvesting profits |

| IP Box | 5% on qualifying IP income | R&D, software and IP-driven businesses |

| Holding / participation exemptions | Potential exemption for qualifying dividend or share-disposal flows, subject to conditions | International holding structures |

The practical takeaway is simple: Poland does not win only on the nominal CIT rate. It wins when the entry structure, investment location, incentive eligibility and repatriation strategy are aligned from the beginning.

Commercial note: many foreign investors lose time or value by reviewing incentives too late. If you are considering Poland seriously, it is worth checking tax eligibility before choosing the entity model, the region, or the operational footprint. Talk to Intertax before launch if you want that assessment done in one workstream.

3. Skilled and Cost-Competitive Workforce

Poland’s labour market remains one of its strongest advantages. Statistics Poland reported 17.9 million economically active people in the third quarter of 2025, including 17.4 million employed persons. That scale matters because it gives investors more room to hire beyond a single-city strategy.

The education pipeline is also meaningful. Statistics Poland reported about 1.28 million students in higher education in the 2024/2025 academic year, with business, administration, law, engineering, health, and social sciences all strongly represented. For employers building finance, IT, engineering, multilingual support, or compliance functions, the practical implication is a wider recruitment base than in many smaller CEE markets.

Poland’s business services sector adds another layer of proof. ABSL reports 2,081 business services centres in Poland, employing nearly half a million people. That shows Poland is no longer just a destination for basic back-office processing. International groups are building multifunctional, knowledge-intensive operations in finance, technology, analytics, cybersecurity and R&D.

Cost remains part of the story, but it should be framed carefully. Poland is not a bargain-basement location, and wages have been rising. Even so, labour costs remain materially below those in Western Europe’s largest markets, while the available talent base is deeper than in many neighbouring jurisdictions. For foreign investors, that often means a better quality-to-cost ratio and a lower risk of running out of talent immediately after launch.

4. Macroeconomic Stability and EU Membership

Poland’s investment case is stronger because it rests on macroeconomic resilience rather than a single short-term trend. Historically, Poland is widely known as the only EU country to avoid recession in 2009. More importantly for a 2026 decision-maker, OECD projections still point to positive growth in both 2025 and 2026, even in a more difficult European environment.

EU membership remains central to the case. Investors gain access to the single market, common regulatory frameworks, and a deep legal and trade architecture that reduces market-entry friction compared with non-EU jurisdictions. That matters for customs positioning, VAT planning, movement of goods, and broader board-level risk assessment.

OECD projections also keep Poland below the Maastricht 60% of GDP debt reference value in 2026, even though fiscal policy should still be monitored closely. Security considerations matter too. Poland’s NATO membership, major defence spending, and regional role after Russia’s full-scale invasion of Ukraine have increased its strategic importance for companies reassessing Eastern European exposure.

For many management teams, the conclusion is practical rather than symbolic: Poland offers a stronger mix of growth, market access, and institutional predictability than a purely cost-led comparison would suggest.

5. Large and Growing Consumer Market

Poland is not only an export platform. It is also one of the European Union’s larger domestic markets. Eurostat’s Poland-in-the-EU snapshot published in January 2025 used a population base of 36.6 million inhabitants, which still places Poland among the biggest consumer markets in the region and gives investors a domestic demand story that smaller CEE markets cannot match.

That scale gives foreign companies more than one route to growth. You can launch in Poland to serve local customers, but also use the country as a commercial and operating base for wider regional expansion. This is especially relevant for industrial distribution, e-commerce, consumer products, B2B services and multi-market fulfilment models.

Poland’s urban structure also helps. Instead of relying on one capital-city market only, companies can build around several strong business centres with different labour, logistics and customer profiles. For investors, that means more flexibility and less concentration risk.

6. Grants, Subsidies and Beyond-Tax Incentives

Tax incentives are only part of the support landscape. Investors should also review grants, EU co-financing, recruitment and training support, and location assistance. Depending on the project, programmes linked to the 2021-2027 EU funding cycle may offer relevant support, including instruments under FENG, FEnIKS, and FEPW.

PAIH, the Polish Investment and Trade Agency, remains one of the most useful first-stop institutions for foreign investors comparing locations, permits, sectors, and public support. Its role is not to replace tax or legal structuring, but it can accelerate early-stage site selection and incentive mapping. In parallel, workforce-related support may be available through training and upskilling channels such as BUR, depending on region and programme conditions.

The key commercial point is timing: grants and subsidy mapping should happen alongside tax structuring, not after the legal vehicle is already chosen. Current public-investment support options can be explored directly on PAIH’s Why Poland page.

7. Key Investment Sectors in Poland (2026)

- IT, AI and software: Poland remains one of the region’s strongest technology talent pools for engineering, product development, cybersecurity, and enterprise support.

- BPO, SSC, GBS and R&D: Krakow, Wroclaw, Warsaw, the Tri-City, Katowice and Poznan continue to attract higher-value shared-services and knowledge-process operations.

- Green energy: Offshore wind, grid modernisation, industrial decarbonisation, and solar-related investments continue to create opportunities for suppliers and project partners.

- Defence and dual-use manufacturing: Poland’s record defence spending is supporting procurement, industrial partnerships, and broader security-related supply chains.

- Logistics and e-commerce: Poland’s location, warehousing base, and cross-border connectivity make it a natural fulfilment and distribution hub for the CEE region.

- Biotechnology and pharmaceuticals: Investors are also active in life sciences, contract manufacturing, and specialised healthcare-related operations.

8. How to Enter Poland More Efficiently

The companies that move into Poland most smoothly usually make a few decisions early. They check whether a local entity is really needed, assess VAT exposure before invoicing starts, review payroll and employment obligations before hiring, and test whether incentives should shape the location or group structure.

- Decide whether you need a company, branch, VAT registration only, or another operating model.

- Review CIT, VAT, withholding tax and payroll exposures before launch.

- Assess whether the Polish Investment Zone or other support can improve project economics.

- Plan compliance early for accounting, payroll, reporting and KSeF-related workflows.

- Align the legal setup with the commercial plan, not the other way around.

Our more detailed guide on entering the Polish market can help you map the full process.

9. FAQ

Is Poland a good country to start a business as a foreigner?

Yes, especially if you need EU market access, a sizeable labour pool, and room to scale beyond one city. Poland is usually strongest for investors who treat it as a strategic operating base rather than a short-term low-cost location.

What taxes will a foreign company pay in Poland?

That depends on the structure and activities. The standard CIT rate is 19%, with a 9% rate available for eligible smaller taxpayers. VAT, withholding tax, payroll taxes, transfer pricing, and permanent-establishment issues may also apply depending on the model.

How does the Polish Investment Zone work?

The Polish Investment Zone allows eligible investors to obtain income tax relief for qualifying new investments across Poland. Relief depends on region, company size, project type, and meeting the conditions in the support decision.

Is Poland safe for long-term investment given the war in Ukraine?

Poland remains one of the region’s key NATO states and has significantly increased defence spending. That does not remove geopolitical risk, but it does make Poland a more strategically anchored location than many investors assume at first glance.

What is the minimum share capital to open a company in Poland?

For a standard Polish limited liability company (sp. z o.o.), the minimum share capital is PLN 5,000. Other entry models, such as branches or representative offices, follow different rules and should be assessed case by case.

10. How Intertax Can Help You Enter the Polish Market

Intertax supports foreign businesses with VAT registration, company formation, tax advisory, payroll, fiscal representation, and e-invoicing readiness, including KSeF-related compliance planning. We help investors turn a broad “why Poland?” discussion into an execution plan with the right structure, the right compliance setup and fewer surprises after launch.

- Company setup and registration planning

- VAT registration and ongoing VAT compliance

- Corporate tax advisory and market-entry structuring

- Payroll and employment compliance support

- Fiscal representation and e-invoicing / KSeF readiness

Book a free initial consultation if you want to assess your market-entry path. You can also review our services or start with our guide on entering the Polish market.