Executive Summary

In Poland, the cost of hiring an employee is always higher than the gross salary stated in the employment contract. For a standard employment contract in 2026, employers should usually expect total direct monthly cost to equal gross salary plus around 20% in statutory employer-side charges, and more if PPK and benefits apply. For example, a salary of 10,000 PLN gross typically means about 6,929 PLN net for the employee and about 12,198 PLN in direct employer cost when standard assumptions include PPK.

Why the “Salary” Is Never the Full Picture

Many foreign employers entering Poland assume that the salary discussed with a candidate is the full cost of employment. In practice, that is only one layer of the picture. In Poland, an employment contract usually states a *gross salary, but the employee receives a lower net salary, while the employer pays a higher total employment cost* once mandatory employer-side charges are added.

This distinction matters for budgeting, payroll planning, and headcount forecasting. A gross salary that looks straightforward in the contract may translate into a much lower take-home amount for the employee and a noticeably higher real cost for the employer. In this guide, we explain the full payroll structure for 2026, show how gross, net, and employer cost relate to each other, and highlight the extra cost areas foreign companies often miss.

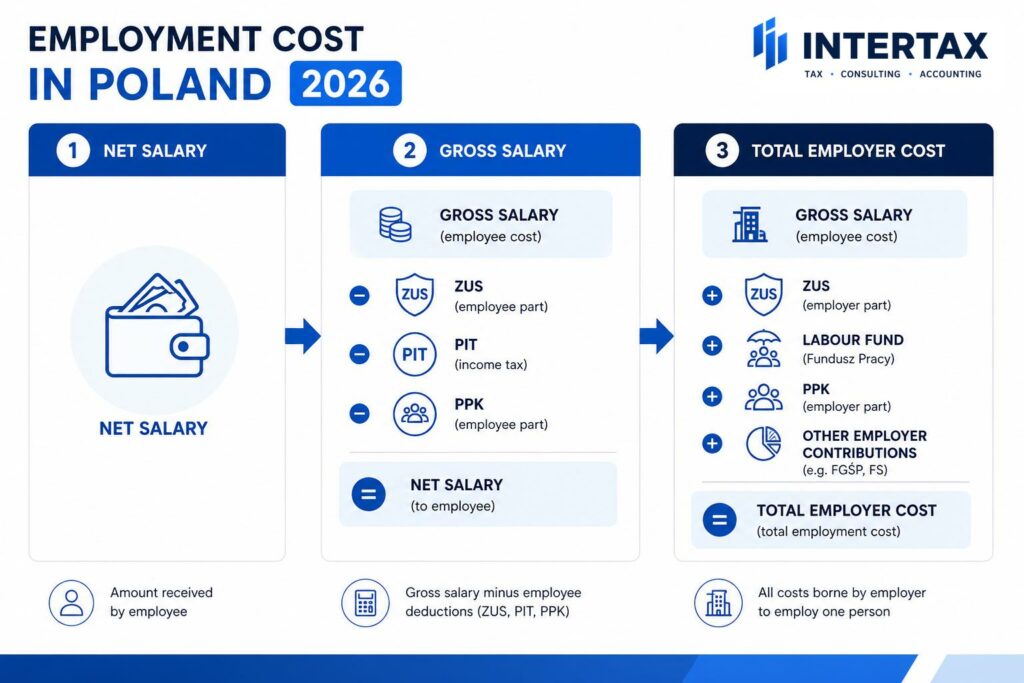

The Three Layers of Employment Cost in Poland

To understand the cost of hiring an employee in Poland, it is useful to break payroll into three separate layers.

- Net salary is the amount the employee actually receives in their bank account. This is what remains after employee social contributions, health insurance, PIT advance, and any employee PPK contribution are deducted.

- Gross salary is the salary stated in the employment contract. In Poland, this is the standard contractual reference point for employment relationships. It is neither an annual package figure nor a net guarantee. It is the payroll base from which employee deductions and many employer-side costs are calculated.

- Total employer cost is the employer’s real direct cost. It includes gross salary plus mandatory employer-financed contributions, such as pension, disability, accident insurance, Labour Fund, FGSP, and PPK where applicable.

This is an important practical difference from some Western markets, where compensation conversations often focus on annual packages or expected net pay. In Poland, employment contracts and payroll administration are built around gross salary. If an international group budgets only for the gross amount written in the contract, the hiring forecast will usually be too low.

What the Employee Pays – Deductions from Gross Salary

Before an employee receives take-home pay, several mandatory deductions are made from gross salary. Under a standard employment contract, the employee usually finances the following social contributions:

- Pension contribution: *9.76%*

- Disability contribution: *1.50%*

- Sickness contribution: *2.45%*

After these social contributions are deducted, the employee also pays *health insurance at 9%* of the relevant contribution base. For employees, that base is reduced by the employee-financed social contributions.

The next deduction is the *PIT advance. Under the standard Polish tax scale, income is taxed at 12% up to 120,000 PLN annually and 32% above that threshold. In a standard payroll setup, the monthly PIT calculation is also affected by the tax-free amount and employee tax-deductible costs. In many ordinary employment cases, this means a monthly tax-reducing amount of 300 PLN if the employee has filed the relevant declaration, and standard employee tax-deductible costs of 250 PLN per month*.

PPK may reduce net salary further. The basic employee PPK contribution is typically *2%*, unless the employee opts out or qualifies for a reduced basic rate under the statutory rules. It is also worth remembering that employer PPK contributions increase the employee’s taxable income for PIT purposes, so PPK can affect both net pay and total employer cost at the same time.

There are special cases as well. For example, the PIT zero relief for people under 26 can materially improve the employee’s net result. This is why any salary example should be read as a model based on stated assumptions, not as a universal payroll result for every worker.

What the Employer Pays – Contributions on Top of Gross

This is the key point for foreign employers: in Poland, the employer pays mandatory charges *on top of* the gross salary stated in the employment contract.

For a standard employment relationship, employer-side costs typically include:

- Pension contribution: *9.76%*

- Disability contribution: *6.50%*

- Accident insurance: typically *1.67%* for small employers, although the rate may vary depending on profile and headcount

- Labour Fund: *2.45%*

- FGSP: *0.10%*

- PPK employer basic contribution: *1.5%* where applicable

Without PPK, that standard employer-side burden is usually just over *20%* of gross salary when the accident rate is assumed at 1.67%. If the employer finances the basic PPK contribution, the effective direct cost rises further.

There is also an important annual threshold for higher earners. In 2026, the annual cap for pension and disability contribution base, commonly referred to as the 30-times cap, is *282,600 PLN*. Once an employee exceeds that annual base, pension and disability contributions stop for the remainder of the year. This can reduce the effective cost percentage for higher salaries later in the year.

In other words, the gross salary should never be treated as the full hiring budget. If the contract says 10,000 PLN gross, the company’s actual monthly payroll cost is meaningfully higher even before optional benefits, bonuses, medical packages, or onboarding costs are added.

Real-World Example – Full Cost Breakdown for 2026

The examples below use one consistent payroll scenario: standard tax-deductible employee costs, PIT-2 applied, employee PPK at 2%, employer PPK at 1.5%, and accident insurance at 1.67%.

Example 1: Minimum wage employee – 4,806 PLN gross

| Element | Amount (PLN) |

| Gross salary | 4,806.00 |

| Employee ZUS contributions | 658.91 |

| Employee health insurance | 373.24 |

| PIT advance | 176.00 |

| Employee PPK contribution | 96.12 |

| Net salary (take-home) | 3,501.73 |

| Employer ZUS contributions | 861.72 |

| Labour Fund + FGSP | 122.56 |

| PPK (employer) | 72.09 |

| Total employer cost | 5,862.37 |

For every 4,806 PLN gross written in the contract, the employee receives approximately 3,502 PLN net, while the employer’s direct monthly cost is approximately 5,862 PLN.

Example 2: Specialist role – 10,000 PLN gross

| Element | Amount (PLN) |

| Gross salary | 10,000.00 |

| Employee ZUS contributions | 1,371.00 |

| Employee health insurance | 776.61 |

| PIT advance | 723.00 |

| Employee PPK contribution | 200.00 |

| Net salary (take-home) | 6,929.39 |

| Employer ZUS contributions | 1,793.00 |

| Labour Fund + FGSP | 255.00 |

| PPK (employer) | 150.00 |

| Total employer cost | 12,198.00 |

For every 10,000 PLN gross written in the contract, the employee receives approximately 6,929 PLN net, and the employer’s direct monthly cost is approximately 12,198 PLN.

Contract Type Matters – How Costs Change

The legal form of cooperation has a major impact on cost structure in Poland. A standard employment contract is only one option, and it is usually the most protective for the worker and one of the most expensive for the employer.

*Employment contract* means full payroll obligations, broad employee protection, paid leave, sick-pay rules, and the clearest compliance framework. It is usually the highest-cost standard model for the employer.

*Umowa zlecenie, often translated as a contract of mandate, can also trigger ZUS obligations, although the exact cost profile depends on the person’s status and other titles to insurance. A common exception concerns many students under 26. In 2026, the statutory minimum hourly rate for relevant civil-law contracts is 31.40 PLN gross*.

*B2B cooperation* is not employment in the formal sense. The contractor handles their own taxes and social security, so the engaging company may see a lower direct cost. However, this lower headline cost comes with a different risk profile. If the arrangement resembles employment in practice, the relationship may be challenged from a labour-law or social-security perspective.

*Umowa o dzieło* may be lighter from a ZUS perspective in some situations, but its legal use is narrower and should not be treated as a universal substitute for employment.

| Factor | Employment contract | Umowa zlecenie | B2B |

| Employer ZUS | Usually around 20%+ | Often applies | None on employer side |

| PPK | Yes | May apply depending on status | No |

| Minimum wage/rate | 4,806 PLN/month | 31.40 PLN/hour | N/A |

| Employee protection | Highest | Lower | Commercial relationship |

| Reclassification risk | Very low | Lower than B2B, fact-dependent | Higher if it resembles employment |

For international employers, the cheapest model on paper is not always the lowest-risk option in practice.

Hidden Costs Foreign Employers Often Overlook

Mandatory payroll contributions are only one part of the real hiring budget. Foreign employers often underestimate the operational and compliance costs attached to local employment in Poland.

- *Paid annual leave: employees are generally entitled to 20 or 26 days* of annual leave depending on tenure.

- *Public holidays:* paid non-working public holidays affect real working-time cost.

- *Sick pay: the employer finances sick pay for the first 33 days of incapacity in a calendar year, or 14 days* for employees aged 50+.

- *Medical exams:* pre-employment, periodic, and control medical exams are financed by the employer.

- *BHP training:* mandatory health and safety training takes place at the employer’s cost.

- *Severance exposure:* in some redundancy situations, severance may apply.

- *PFRON exposure:* employers with at least 25 FTE may face additional obligations if disability-employment thresholds are not met.

- *Voluntary but expected benefits:* depending on the package, benefits may add a noticeable extra cost.

These items are easy to miss when a company compares salary offers across countries. On paper, payroll may look simple. In reality, the full cost of hiring in Poland includes both statutory payroll charges and the broader cost of maintaining a compliant employment relationship.

Key 2026 Updates That Affect Your Costs

Several 2026 points are especially relevant for employers planning headcount in Poland.

- *Minimum wage: from 1 January 2026, the monthly minimum wage is 4,806 PLN gross*.

- *Minimum hourly rate: from 1 January 2026, the minimum hourly rate for relevant civil-law contracts is 31.40 PLN gross*.

- *30-times cap: the annual cap for pension and disability contributions in 2026 is 282,600 PLN*.

- *Entrepreneur health contribution context: from February 2026, the minimum health contribution for certain entrepreneurs reaches 432.54 PLN*, which is relevant when comparing B2B economics with employment.

- *Salary transparency rules: since 24 December 2025*, employers must provide candidates with information on the proposed salary or salary range in the recruitment process, in writing, at the latest before the employment relationship is formed. In practice, many employers will choose to publish this in the job ad, but the legal obligation is broader than the ad itself.

- *Recruitment process changes:* the same rules also reinforce non-discriminatory recruitment language and limit the ability to ask candidates about current or past pay.

- *Broader pay transparency implementation:* the wider EU pay transparency framework continues to shape employer obligations in 2026, especially around pay-setting logic, internal consistency, and reporting readiness.

This is one reason older Poland hiring guides written for 2024 or 2025 are often no longer sufficient for current budgeting decisions.

How to Estimate Your Total Hiring Budget

If you want a practical budgeting model, start with the gross salary you expect to offer and then add the other cost layers in a structured way.

- Set the expected *gross monthly salary* based on market conditions for the role and seniority.

- Add roughly *20.5%* for statutory employer-side payroll charges in a standard model.

- Add *1.5%* if you want to include the basic employer PPK contribution.

- Add the expected cost of benefits and allowances.

- Add onboarding and compliance costs such as medical exams, training, equipment, and internal setup.

A practical shortcut is: Total monthly cost ≈ gross salary x 1.22 + benefits

This is a useful high-level planning formula, not a substitute for a payroll review. Final numbers may differ depending on declarations, PPK participation, exemptions, contract type, and the employee’s personal tax status. For a quick orientation, you can compare assumptions with an external payroll calculator such as a Poland salary calculator .

FAQ

How much does it cost to hire an employee in Poland in 2026?

For a standard employment contract, the total employer cost is usually the gross salary plus around 20% in mandatory employer-side charges, and more if PPK and benefits apply. At the 2026 minimum wage of 4,806 PLN gross, the direct employer cost is about 5,862 PLN per month in a standard example with PPK.

What is the difference between gross and net salary in Poland?

Gross salary is the contractual amount stated in the employment contract. Net salary is what the employee actually receives after employee social contributions, health insurance, PIT advance, and any employee PPK contribution are deducted.

What ZUS contributions does an employer pay in Poland?

The employer typically pays pension contribution at 9.76%, disability contribution at 6.5%, accident insurance at a rate depending on employer profile, plus Labour Fund and FGSP. In many standard hiring models, the direct employer-side burden is slightly above 20% of gross salary before PPK.

Is it cheaper to hire on B2B than employment contract in Poland?

From a direct employer-cost perspective, B2B can look cheaper because the company does not pay employer-side payroll contributions in the same way. However, B2B is not a like-for-like replacement for employment and may carry legal and social-security risk if the relationship functions like employment in practice.

What is the ZUS contribution cap (30-krotność) in 2026?

The annual cap for pension and disability contribution base in 2026 is *282,600 PLN*. Once that threshold is exceeded, those two contributions stop for the rest of the year, which can reduce the effective cost percentage for higher earners later in the year.

Next steps

If you are planning to hire in Poland, the safest approach is to model every role from three angles at once: employee net pay, contract gross salary, and full employer cost. That gives finance, HR, and management one shared budgeting framework from the start.

If you want to estimate your real payroll cost in Poland before making an offer, contact INTERTAX for support with payroll setup, employment-cost modelling, and employer compliance.

Related support:

- PIT – personal income tax

- payroll services in Poland

- HR support for foreign employers

- posting workers vs local hiring in 2026

- employee benefits in Poland

- entering the Polish market

Sources

- MRPiPS minimum wage

https://www.gov.pl/web/rodzina/minimalne-wynagrodzenie-za-prace

- MRPiPS minimum hourly rate

https://www.gov.pl/web/rodzina/minimalna-stawka-godzinowa

- Monitor Polski

https://monitorpolski.gov.pl/M2025000120601.pdf

- podatki.gov.pl

- mojePPK / MF

https://www.mojeppk.pl/dla-pracodawcy.html

- PIP

- PIP

https://www.pip.gov.pl/aktualnosci/pora-na-przejrzystosc-wynagrodzen?tmpl=print%3Ftmpl%3Dpdf