If your company sells goods or provides services in Poland and invoices in EUR, USD, or another foreign currency, you need to know these rules to stay compliant. This guide is for business owners, finance teams, accountants, and foreign companies operating on the Polish market who want to avoid costly VAT errors, payment mismatches, and reporting problems.

You will learn when foreign currency invoicing is allowed, how to convert amounts correctly for VAT purposes, what exchange rates to use, and how to handle payments under Polish tax and accounting rules. Whether you issue only occasional cross-border invoices or manage high volumes of international transactions, understanding these requirements will help you reduce risk, improve internal processes, and ensure your invoices meet Polish compliance standards.

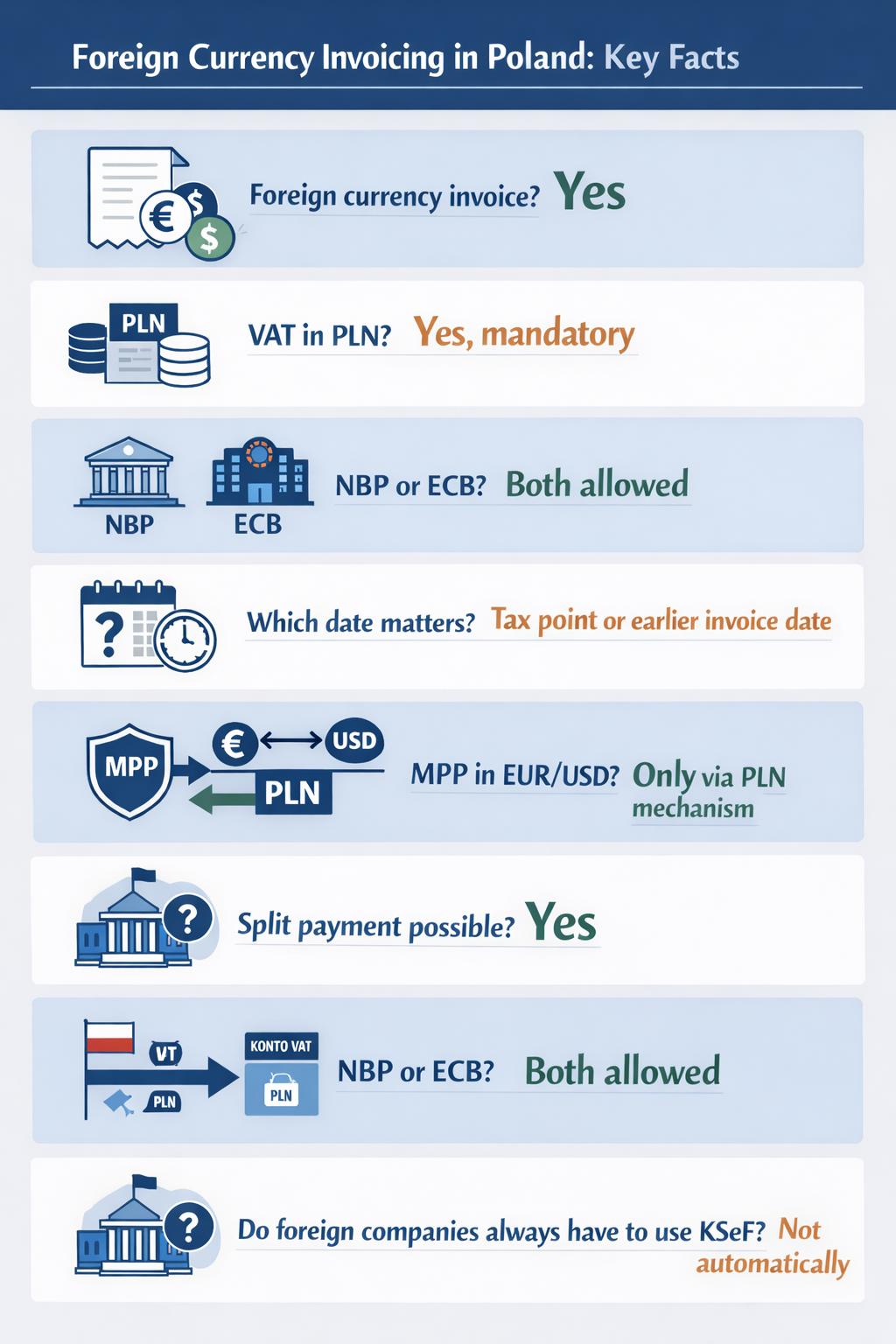

Executive Summary

Under Polish tax regulations, invoices can be issued in foreign currencies, provided that the VAT amount is clearly stated in Polish Zloty (PLN) based on official NBP or ECB exchange rates. While payments are generally made to the bank account specified by the issuer, the Split Payment Mechanism (MPP) becomes mandatory for B2B transactions exceeding PLN 15,000 that involve specific “sensitive” goods or services. For foreign entities without a fixed place of business in Poland, maintaining a Polish bank account is only required if their activities fall under these mandatory split payment obligations.

Can You Issue Invoices in Foreign Currency in Poland?

Yes. Under Polish VAT rules, invoices may be issued in a foreign currency such as EUR, USD, or GBP. However, if the invoice shows VAT, the VAT amount must be stated in PLN, even where the net value or gross commercial amount is expressed in a foreign currency. In practice, this means a business may invoice in foreign currency for commercial purposes, but it must still apply the Polish VAT conversion rules for tax reporting. The legal basis comes from the Polish VAT Act, which allows invoice amounts to be stated in a foreign currency while requiring the tax amount to be shown in złoty.

For businesses trading internationally, this is a useful and common solution: the contract and payment may be handled in foreign currency, while the tax side remains aligned with Polish compliance requirements.

The key is to ensure that the exchange rate is determined correctly and that the VAT is reported in PLN where required.

How to Convert VAT to PLN – NBP and ECB Exchange Rates

Under Polish VAT rules, amounts shown on an invoice may be expressed in a foreign currency, but the VAT amount must be converted into PLN for tax reporting purposes.

As a rule, the conversion should be made using the average exchange rate published by the National Bank of Poland (NBP) on the last working day preceding the date when the tax point arises. Alternatively, taxpayers may choose the exchange rate published by the European Central Bank (ECB), provided this method is applied consistently.

If the ECB does not publish a rate for a given currency, conversion should first be made via EUR. Choosing the correct rate and applying it at the right moment is essential, because errors in VAT conversion may lead to discrepancies in the JPK_V7 return and create unnecessary compliance risks during a tax audit.

Which exchange rate to use (NBP vs ECB)

In Poland, the default rule is to use the average exchange rate published by the National Bank of Poland (NBP) on the last working day preceding the date when the VAT liability arises. If the invoice is issued before the tax point, the conversion is generally made using the NBP rate from the last working day preceding the invoice date.

As an alternative, taxpayers may use the exchange rate published by the European Central Bank (ECB), but only if this approach is adopted consistently. Where the ECB does not publish a direct rate for a given currency, the amount should first be converted into EUR.

In practice, NBP is the standard and most commonly used method in Poland, while ECB may be helpful for businesses that operate within EU-wide accounting or invoicing systems. The key point is not which method looks more favourable on a given day, but that the chosen method is legally permitted and applied consistently.

Date of the exchange rate – tax point vs invoice date

As a rule, for Polish VAT purposes you use the exchange rate from the last working day preceding the date when the VAT liability arises. That means the tax point is the default reference date, not the payment date and not automatically the invoice date.

However, if you issue the invoice before the VAT liability arises, and the taxable amounts are already stated in a foreign currency on that invoice, then you use the rate from the last working day preceding the invoice date instead. The same timing logic applies whether you use the NBP average rate or, if chosen consistently, the ECB rate. In practice, this means: if the service was performed first and the invoice was issued later, look to the tax point; if the invoice was issued in advance, look to the invoice date.

Practical example: EUR invoice with VAT conversion

A Polish company provides consulting services to a client in Poland for EUR 1,000 net plus 23% VAT. The service is performed on 15 March, and the invoice is issued on 18 March. Because the invoice was issued after the VAT point arose, the relevant exchange rate is the average NBP rate from the last working day preceding 15 March. If that rate is 1 EUR = PLN 4.30, the taxable base for VAT purposes is PLN 4,300.00, and the VAT amount is PLN 989.00 (23% of PLN 4,300.00).

On the invoice, the seller may still show the commercial amounts in euro — EUR 1,000 net and EUR 230 VAT — but for Polish VAT reporting, the VAT must be converted into PLN using the correct statutory exchange rate.

If the taxpayer has validly opted for the ECB method instead, the same timing rule applies, but the ECB rate must be used consistently.

NBP vs ECB Exchange Rate for Polish VAT – Comparison Table

When issuing invoices in a foreign currency in Poland, taxpayers must convert VAT amounts into PLN for reporting purposes. The NBP rate is the default method under Polish VAT rules, while the ECB rate may be used as an alternative if applied consistently.

Although the difference in value is often small, the chosen method affects the taxable base and VAT amount in PLN.

| Criterion | NBP Exchange Rate | ECB Exchange Rate |

| Status under Polish VAT law | Default method | Optional alternative |

| Rate source | National Bank of Poland | European Central Bank |

| Reference date | Last working day preceding the tax point, or the invoice date if the invoice is issued earlier | Same rule |

| Typical use in practice | Most commonly used by Polish businesses | Often used by international groups for internal consistency |

| Consistency requirement | Standard statutory approach | Must be applied consistently once chosen |

| Non-EUR currencies | Used if published by NBP | If no direct ECB rate exists, conversion is made via EUR |

| Main advantage | Familiar to Polish accountants and tax authorities | Useful for businesses using EU-wide finance policies |

Numerical Example – NBP vs ECB

Assume a Polish company issues an invoice for:

- Net amount: EUR 10,000

- VAT rate: 23%

- Applicable conversion date: 9 April 2026

For illustration, assume the following exchange rates apply:

- NBP rate: 1 EUR = PLN 4.2623

- ECB rate: 1 EUR = PLN 4.2558

VAT conversion result

| Calculation | NBP Method | ECB Method |

| Net amount | EUR 10,000.00 | EUR 10,000.00 |

| Exchange rate | 4.2623 | 4.2558 |

| Net amount in PLN | PLN 42,623.00 | PLN 42,558.00 |

| VAT rate | 23% | 23% |

| VAT in PLN | PLN 9,803.29 | PLN 9,788.34 |

In this example, the NBP method produces a VAT amount that is PLN 14.95 higher than the ECB method. The difference is not large, but it shows why businesses should choose their method carefully and apply it consistently in practice.

Suggested note

For most Polish taxpayers, the NBP rate remains the safest and most practical choice. However, businesses operating across multiple EU jurisdictions may prefer the ECB rate to align their invoicing and accounting systems. The most important rule is consistency: once the ECB method is chosen, it should be used systematically.

Paying for Foreign Currency Invoices in Poland

Paying a foreign currency invoice in Poland is generally allowed, but businesses must still pay close attention to VAT, accounting, and banking implications. Even if an invoice is issued and settled in EUR, USD, or another currency, Polish tax reporting may still require certain amounts, especially VAT, to be reflected in PLN.

Companies should also verify whether the payment method complies with Polish business payment rules, including the use of bank transfers in transactions above statutory thresholds and, where applicable, the white list and split payment mechanisms. In practice, the currency of payment does not remove compliance obligations — it only adds another layer of exchange rate, documentation, and reconciliation issues that must be handled correctly.

Bank account requirements for foreign sellers

A foreign seller may issue invoices to Polish customers in a foreign currency and receive payment to a foreign bank account, but the Polish white list rules matter if that seller is registered in Poland as an active VAT taxpayer.

In that case, the foreign business is treated like a Polish active VAT taxpayer, and its settlement account should be disclosed in the VAT white list. By contrast, if the foreign seller uses a foreign VAT identification number for the transaction and is not acting under a Polish NIP for that sale, it is not required to open a Polish settlement account just to have it shown on the white list, and the buyer does not apply the white-list account verification rules to that payment.

The Ministry of Finance also states that foreign bank accounts are not shown on the white list, because the list contains only Polish settlement accounts or certain SKOK accounts meeting statutory criteria. In addition, split payment (MPP) applies only to PLN bank transfers made to other VAT taxpayers, so it does not work in the usual way for a foreign-currency payment made to an ordinary foreign account.

A practical takeaway is this: if a foreign seller is Polish VAT-registered and invoicing a Polish domestic supply, using a properly reported Polish business settlement account is usually the safest option for large B2B payments.

If the seller is not Polish VAT-registered for that transaction, payment to a foreign bank account is generally possible without white-list consequences for the Polish buyer.

White List verification

Before paying a Polish supplier, the buyer should verify two things in the VAT White List, first, whether the seller is listed with the relevant VAT status on the chosen date, and second, whether the bank account to be paid appears in the register for that taxpayer.

The register is maintained electronically by the Head of the National Revenue Administration and can be searched by NIP, company name fragment, REGON, or bank account number, always for a specific date. The official search also allows verification of historical data for dates falling within the last 5 years.

In practice, for a domestic B2B payment in Poland, the safest approach is to check the supplier’s NIP + account number on the day you order the transfer and keep proof of that verification, because the register is designed precisely for confirming whether the account disclosed by the supplier is one of the accounts shown in the VAT register on that date.

The White List contains, in particular, settlement accounts and certain SKOK accounts confirmed through STIR; it is not a general list of every possible account used by a business.

A practical point for foreign-currency and international payments is that the White List mechanism is mainly relevant where Polish law expects payment to a disclosed account of a taxpayer visible in the Polish VAT register.

If the account is not the type of account disclosed in the register, or the seller is not shown there for that transaction, the buyer should assess separately whether White List consequences arise and whether another protective step is needed.

Consequences of paying to an account not listed on the White List

If a Polish B2B payment above PLN 15,000 is made by transfer to a supplier’s account that is not shown on the VAT White List, the buyer may face two main risks: the expense may be excluded from tax-deductible costs for PIT/CIT purposes, and the buyer may incur joint and several liability for the supplier’s VAT arrears connected with that transaction. These risks can generally be neutralised by filing a ZAW-NR notification within 7 days from the date of the transfer order.

So, in practical terms: if the account is missing from the White List, either do not pay until the issue is clarified, or file ZAW-NR on time to preserve protection.

Split Payment Mechanism (MPP) and Foreign Currency Invoices

When is split payment mandatory?

In Poland, mandatory split payment (MPP) applies only if all of the following conditions are met: the transaction is B2B, the invoice covers goods or services listed in Appendix 15 to the Polish VAT Act, and the gross invoice amount exceeds PLN 15,000 (or the equivalent in foreign currency). In that case, the seller should mark the invoice with “mechanizm podzielonej płatności”, and the buyer must pay using the split payment mechanism.

A key practical point is that MPP works through a Polish bank transfer that splits the payment between the seller’s regular business account and its VAT account, so in practice it is designed for payments made through Polish business banking infrastructure.

That is why it is mainly relevant to domestic Polish VAT transactions rather than ordinary foreign transfers to overseas accounts.

So the short rule is: MPP is mandatory only for Appendix 15 goods/services on an invoice above PLN 15,000 gross. In other cases, split payment may still be used voluntarily, but it is not compulsory.

Split payment for invoices in EUR/USD – is it possible?

Yes, but only in a limited sense. A Polish invoice may be issued in EUR, USD, or another foreign currency, and it may still fall under mandatory split payment if the usual conditions are met, such as a B2B transaction, goods/services from Appendix 15, and an invoice value above PLN 15,000 equivalent. However, the split payment transfer itself can be made only in PLN and only through the Polish split-payment banking mechanism to another VAT taxpayer’s account with an associated VAT account.

So the practical rule is this: an invoice may be denominated in EUR or USD, but if you want to use MPP, the payment message operates in PLN, not in foreign currency. In other words, foreign-currency invoicing is possible, but a classic EUR-to-EUR or USD-to-USD bank transfer is not itself an MPP payment.

This is why MPP is mainly workable where the seller has the Polish banking setup needed for split payment. If the transaction is one that would otherwise require mandatory MPP, but the payment is made as an ordinary foreign transfer in EUR/USD outside that mechanism, that creates a compliance risk.

What if the seller has no Polish bank account?

That is the practical problem: split payment can only work through a Polish settlement account linked to a VAT account, because the net amount goes to the seller’s settlement account and the VAT amount goes to the seller’s special VAT account. An ordinary foreign account does not support this mechanism.

So if an invoice is one for which mandatory MPP applies, but the seller has no Polish bank account capable of receiving split payment, the buyer cannot properly perform a compliant MPP transfer in the normal way. In practice, that means the parties should not treat a standard foreign transfer as a substitute for MPP.

The safer conclusion is that the seller should first arrange the banking setup needed for MPP, or the transaction structure should be reviewed before payment.

Also, if the seller is a Polish active VAT taxpayer, the White List system is built around accounts shown in that register, and the published accounts are Polish settlement accounts or certain SKOK accounts, not ordinary foreign accounts.

If mandatory split payment applies, a seller without a Polish settlement account and VAT account creates a compliance problem, because an ordinary foreign transfer in EUR or USD does not satisfy the Polish MPP mechanism.

KSeF and Foreign Currency Invoices (2026 Update)

As of 2026, KSeF is being rolled out in stages: it has been mandatory since 1 February 2026 for taxpayers whose 2024 sales exceeded PLN 200 million, and since 1 April 2026 for other businesses. There is also a transitional simplification until 31 December 2026: invoices may still be issued outside KSeF if, in a given month, the total gross value of such invoices does not exceed PLN 10,000.

For foreign currency invoices, KSeF does not change the core VAT conversion rules. A structured invoice may still be issued in EUR, USD, or another foreign currency, but where the invoice is expressed only in foreign currency, the VAT amount must still be shown in PLN in line with the Polish VAT Act. The KSeF FA(3) structure expressly supports this: for foreign-currency invoices, the invoice uses currency fields such as KodWaluty and KursWaluty, while the VAT amount is shown in PLN.

For foreign sellers, the key question is not the currency of the invoice but whether the business is actually covered by the KSeF obligation in Poland. According to the Ministry of Finance FAQ, a foreign entity registered for Polish VAT is not subject to mandatory KSeF if it has no seat and no fixed establishment in Poland, or if it has a Polish fixed establishment that does not participate in the supply documented by the invoice. Such entities may still use KSeF voluntarily.

So the practical 2026 takeaway is this: you can issue a KSeF invoice in a foreign currency, but Polish VAT still needs PLN treatment, and foreign businesses must first determine whether KSeF is mandatory for them at all

Who must use KSeF?

In 2026, mandatory KSeF applies in stages to taxpayers issuing invoices in Poland. It has applied since 1 February 2026 to businesses whose 2025 sales exceeded PLN 200 million, and since 1 April 2026 to other taxpayers, including sole traders and SMEs. The smallest businesses benefiting from the transitional PLN 10,000 monthly threshold move fully into KSeF from 1 January 2027.

As a practical rule, KSeF is intended for entrepreneurs issuing invoices under Polish invoicing rules. This includes Polish businesses and also certain foreign entities that are within the Polish invoicing scope.

Some foreign businesses are not mandatorily covered. A foreign entity is outside mandatory KSeF if it has no registered seat and no fixed establishment in Poland, or if it has a fixed establishment in Poland but that establishment does not participate in the supply documented by the invoice. Those businesses may still use KSeF voluntarily.

Foreign companies – established vs non-established

For Polish KSeF purposes, the key distinction is whether a foreign company is established in Poland or non-established. A foreign business is generally treated as established if it has a registered seat in Poland or a fixed establishment in Poland that participates in the specific supply documented by the invoice. In that case, it may fall within mandatory KSeF just like a Polish business.

By contrast, a foreign company is usually treated as non-established where it has no seat in Poland and no fixed establishment in Poland, or where its Polish fixed establishment does not participate in the transaction covered by the invoice. In that situation, the company is generally outside mandatory KSeF, although it may still use the system voluntarily.

The practical takeaway is simple: Polish VAT registration alone does not automatically mean mandatory KSeF. What matters is the seller’s level of establishment in Poland and, in particular, whether a Polish fixed establishment is actually involved in the supply.

The Ministry of Finance has also issued tax guidance on how to assess a fixed establishment for KSeF purposes, which shows this is a substantive, fact-based test rather than a purely formal registration question.

How to submit a foreign currency invoice via KSeF

To submit a foreign currency invoice through KSeF, you do not use a separate foreign-currency procedure. You issue a standard structured invoice in the FA(3) format and complete the invoice currency fields, including KodWaluty and, where applicable, KursWaluty. From 1 February 2026, FA(3) is the required structure for invoices issued in KSeF.

The key rule is that the sales and VAT values are generally entered in the currency of the invoice, but the fields relating to VAT converted under the Polish VAT Act must reflect PLN values where Polish law requires that treatment. The FA(3) documentation expressly notes this distinction for foreign-currency invoices.

In practice, the process looks like this: prepare the invoice in your ERP or in the free KSeF Taxpayer Application 2.0, choose the invoice currency, enter the commercial amounts in that currency, calculate VAT in line with the statutory NBP or ECB conversion rules where PLN reporting is required, validate the file against the FA(3) schema, and then send it to KSeF for assignment of a KSeF number.

The Ministry’s free application is expressly intended for issuing, receiving, and viewing invoices compliant with KSeF 2.0.

Common Mistakes When Issuing Foreign Currency Invoices

Foreign currency invoicing in Poland is common, but businesses often make the same avoidable errors.

- One of the most frequent mistakes is assuming that if an invoice is issued in EUR, USD, or another currency, all VAT elements may remain in that currency as well. In practice, the VAT amount still needs to be converted into PLN for Polish tax purposes.

- Another common error is using the wrong exchange rate date — for example, relying automatically on the invoice date when the correct reference point should be the tax point, unless the invoice was issued earlier. Businesses also sometimes switch between NBP and ECB rates without applying one method consistently, which may create compliance risk.

- Other problems arise on the payment side. Taxpayers may overlook White List verification, assume that a foreign bank account is always acceptable for domestic Polish settlements, or ignore the fact that split payment works only through the Polish banking mechanism in PLN.

- In cross-border structures, companies also frequently misjudge whether they are actually covered by mandatory KSeF in Poland. To stay compliant, each foreign currency invoice should be checked not only for its commercial wording, but also for its VAT conversion, payment method, and Polish reporting consequences.

- Wrong invoice wording

Companies sometimes issue a foreign currency invoice without clearly showing all mandatory invoice elements required under Polish VAT rules, including the VAT rate, VAT amount, or legally required annotations. - Showing VAT only in a foreign currency

A common mistake is to present VAT exclusively in EUR or USD, without reflecting the PLN amount where Polish VAT rules require it. - Incorrect rounding

Even when the correct exchange rate is used, errors often arise from improper rounding of the taxable base or VAT amount after conversion into PLN. - Using the payment date instead of the statutory conversion date

Some businesses convert VAT using the date the customer paid, even though the relevant date is generally the tax point or, in some cases, the invoice date if the invoice was issued earlier. - Inconsistency between the invoice and accounting records

The invoice may be correct commercially, but the accounting entry, VAT return, or ERP system may use a different exchange rate or different PLN values. - Ignoring contract and tax mismatch

Businesses often agree prices, payment clauses, or FX adjustment clauses in contracts without checking whether the invoice and VAT treatment follow the same logic. - Confusing accounting FX rules with VAT FX rules

The exchange rate used for accounting or income tax purposes is not always the same as the one required for VAT, and mixing these rules may lead to reporting errors. - Incorrect treatment of advance payments

Where an advance payment is received in foreign currency, businesses sometimes forget that the VAT conversion may need to be determined separately for the advance invoice. - Errors in corrective invoices

Credit notes and debit notes in foreign currency are often handled incorrectly, especially where the original invoice and the correction require separate PLN analysis. - Assuming foreign currency means cross-border treatment

Some taxpayers wrongly assume that invoicing in EUR or USD automatically means the transaction is international, even though the supply may still be fully domestic and subject to Polish VAT rules. - No internal FX policy

Businesses often lack a written internal policy on whether they use NBP or ECB, who verifies rates, and how exceptions are handled, which increases audit risk. - KSeF data inconsistency

In structured invoicing, the commercial currency, VAT values, and technical fields may be entered inconsistently, creating validation or reporting problems.

The biggest risk is not the foreign currency itself, but treating a foreign currency invoice as if it were free from Polish VAT, payment, and reporting rules.

FAQ

1. Can you issue invoices in foreign currency in Poland?

Yes. In Poland, invoices may be issued in foreign currencies such as EUR, USD, or GBP. However, where Polish VAT applies, the VAT amount generally needs to be shown or reported in PLN in accordance with the applicable VAT conversion rules.

2. Which exchange rate should be used for VAT conversion?

The default method is the average exchange rate published by the National Bank of Poland (NBP). Taxpayers may also use the European Central Bank (ECB) rate, but only if that method is chosen and applied consistently.

3. What date determines the exchange rate for VAT purposes?

As a rule, the relevant rate is taken from the last working day preceding the date when the VAT liability arises. If the invoice is issued before the tax point, the rate from the last working day preceding the invoice date is generally used instead.

4. Can a foreign currency invoice be paid to a foreign bank account?

In many cases, yes, especially in cross-border transactions. However, where Polish domestic VAT rules, White List verification, or mandatory split payment apply, using a foreign bank account may create practical and compliance issues.

5. Is split payment possible for invoices issued in EUR or USD?

Yes, but only in a limited way. The invoice itself may be issued in a foreign currency, but the split payment mechanism operates through a Polish bank transfer in PLN, not through a standard EUR or USD transfer.

6. What happens if the supplier’s bank account is not listed on the Polish White List?

If the payment exceeds PLN 15,000 and is made to an account not listed on the White List, the buyer may face negative tax consequences. In practice, this may affect tax deductibility and may also expose the buyer to joint and several liability for the supplier’s VAT arrears, unless corrective steps are taken in time.

7. Do foreign companies always have to use KSeF?

No. A foreign company is not automatically subject to mandatory KSeF just because it is VAT-registered in Poland. The key issue is whether it has a seat in Poland or a fixed establishment in Poland that participates in the invoiced transaction.

8. What is the most common mistake with foreign currency invoices in Poland?

One of the most common mistakes is assuming that if the invoice is issued in EUR or USD, all tax elements may remain in that currency as well. In reality, Polish VAT rules often still require PLN conversion, correct exchange rate timing, and proper reporting treatment.

FAQ – Foreign Currency Invoices in Poland

Can I issue an invoice in EUR or USD to a Polish company?

Yes. In Poland, invoices may be issued in foreign currencies such as EUR or USD, including invoices issued to Polish business customers. However, where Polish VAT applies, the VAT amount generally needs to be shown or settled in PLN for tax purposes.

Which exchange rate should I use – NBP or ECB?

The default method is the average exchange rate published by the National Bank of Poland (NBP). The European Central Bank (ECB) rate may also be used, but only if the taxpayer adopts this method and applies it consistently.

Do I need a Polish bank account to receive payments for invoices?

Not always. A foreign seller may often receive payment to a foreign bank account, but a Polish bank account may become important where Polish White List or split payment rules apply.

Is split payment (MPP) mandatory for foreign currency invoices?

It may be mandatory if the general conditions for MPP are met, such as a B2B transaction, Appendix 15 goods or services, and an invoice amount above PLN 15,000 gross. However, the split payment mechanism itself works through a Polish bank transfer in PLN, even if the invoice is issued in a foreign currency.

Do foreign companies need to use KSeF for invoices in Poland?

Not in every case. A foreign company is generally subject to mandatory KSeF only if it has a seat in Poland or a fixed establishment in Poland participating in the invoiced transaction.

What happens if VAT is not shown in PLN on a foreign currency invoice?

This may create a compliance risk under Polish VAT rules. Even if the commercial invoice is issued in EUR or USD, the VAT amount should generally be reflected in PLN where Polish VAT law requires it.

How do I convert VAT when the invoice date differs from the tax point date?

As a rule, the exchange rate is taken from the last working day preceding the date when the VAT liability arises. If the invoice is issued before the tax point, the rate from the last working day preceding the invoice date is generally used instead.

How Intertax Can Help

Established in 1993, Intertax is a professional firm providing comprehensive tax advisory, accounting and VAT compliance services tailored for international businesses in Poland.

Their team of expert accountants and tax consultants helps foreign investors navigate the complex Polish regulatory environment by offering tax consultation tailored to specific business needs. Additionally, they provide comprehensive VAT services, including registration, compliance, and fiscal representation for non-EU companies.

Key ways Intertax can help your business:

- VAT & Compliance: They manage full VAT services, including VAT registration, reporting, and complex VAT consulting to ensure cross-border transactions meet Polish standards.

- Tax Consultations: Their professionals assist with tax consultation for CIT, PIT, and international tax strategies to minimize legal and fiscal burdens.

- Accounting & Payroll: Intertax provides outsourced accounting services and payroll management, handling bookkeeping and social security (ZUS) contributions.

- Fiscal Representation: For companies based outside the EU, they act as an authorized fiscal representative, taking joint responsibility for Polish VAT obligations.

- Business Support: They offer practical guidance on company formation and e-invoicing (KSeF) implementation for entities entering the Polish market.