Polish Tax Law: A Complete Guide for Foreign Investors (2026)

Polish tax law is important for foreigners because it determines how income, business profits, transactions, investments and cross-border payments are taxed in Poland. For foreign investors, understanding the tax system in Poland is essential before setting up a company, hiring employees, selling goods or services, buying real estate, or receiving income from Polish sources. Poland has one of the more complex, but also relatively predictable, tax systems in Central Europe. Once the correct structure and reporting obligations are identified, tax compliance can usually be managed in a systematic way.

The main taxes affecting companies and individuals include Value Added Tax (VAT), Corporate Income Tax (CIT), Personal Income Tax (PIT) and Withholding Tax (WHT). Depending on the business model, foreign investors may also need to consider tax registration, transfer pricing, payroll taxes, social security contributions, real estate tax and electronic reporting obligations. This guide provides an overview of the key rules of Polish tax law and the practical issues that foreign investors should take into account. The information is prepared with the 2026 tax environment in mind.

Overview of the Polish Tax System

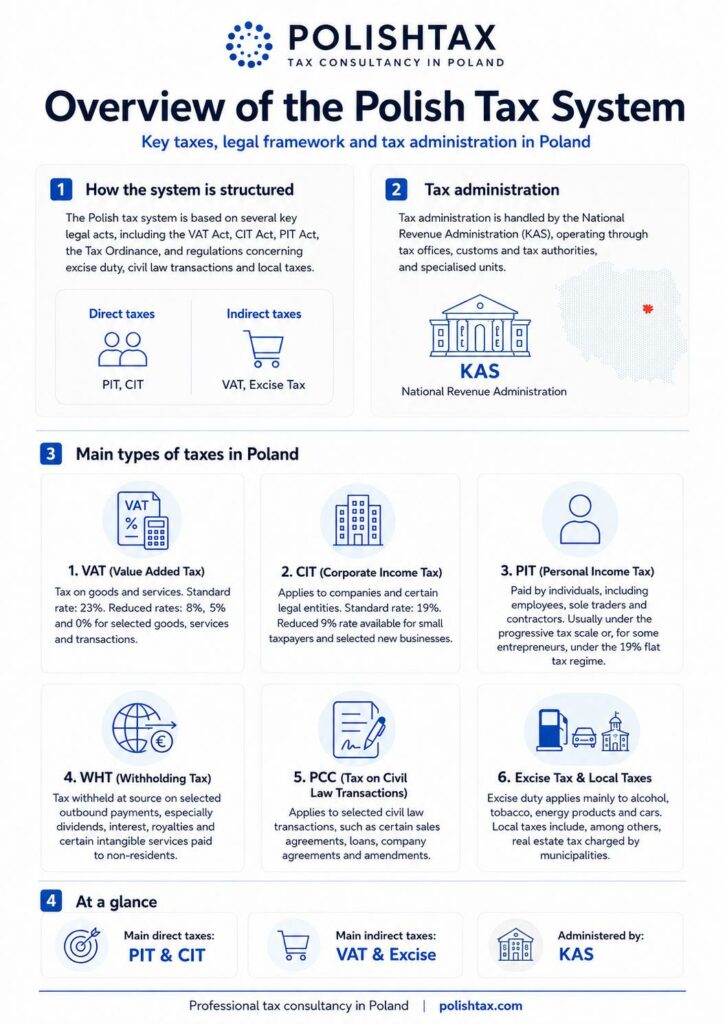

The Polish tax system is structured around several main taxes that apply to companies, individuals and cross-border transactions. It is based on a number of key legal acts, including the VAT Act, CIT Act, PIT Act, Tax Ordinance and regulations concerning excise duty, civil law transactions and local taxes. In practice, types of taxes in Poland are usually divided into direct taxes, such as PIT and CIT, and indirect taxes, such as VAT and excise duty. Tax administration is handled by the National Revenue Administration — Krajowa Administracja Skarbowa (KAS), operating through tax offices, customs and tax authorities and specialised units.

The main types of taxes in Poland include:

- VAT (Value Added Tax) — tax on goods and services, generally charged at 23%, with reduced rates of 8%, 5% and 0% for selected goods, services and transactions.

- CIT (Corporate Income Tax) — corporate income tax imposed on companies and certain other legal entities, usually at 19%, with a reduced 9% rate available for small taxpayers and selected new businesses.

- PIT (Personal Income Tax) — personal income tax paid by individuals, including employees, sole traders and contractors, generally under the progressive tax scale or, for some entrepreneurs, under the 19% flat tax regime.

- WHT (Withholding Tax) — tax withheld at source on selected outbound payments, especially dividends, interest, royalties and certain intangible services paid to non-residents.

- PCC (Tax on Civil Law Transactions) — tax on selected civil law transactions, such as certain sales agreements, loans, company agreements and amendments to those agreements.

- Excise Tax / Local Taxes — excise duty applies mainly to specific goods such as alcohol, tobacco, energy products and cars, while local taxes include, among others, real estate tax charged by municipalities.

Corporate Taxation in Poland – What Every Business Must Know

Corporate income tax Poland rules are particularly important for foreign companies planning to operate, invest, sell goods or provide services in the Polish market. In 2026, CIT Poland generally applies at the standard rate of 19%, while a reduced 9% CIT rate may be available to small taxpayers and certain new businesses. The small taxpayer threshold is generally linked to annual sales revenue not exceeding the equivalent of EUR 2 million, subject to detailed statutory conditions. Polish official business guidance confirms that the CIT rate is 19% or 9% for small taxpayers and new businesses.

A foreign company may become subject to tax on business in Poland if it is considered a Polish tax resident or if it operates in Poland through a permanent establishment. Polish tax residence may arise, in particular, when a company has its registered office or place of management in Poland. A permanent establishment may be created when a foreign business has a fixed place of business in Poland, such as an office, branch, construction site or dependent agent, depending on the facts and the relevant double tax treaty.

For investors, Poland also offers tax incentives that may reduce the effective tax burden. One of the most important is the R&D tax relief, which allows eligible research and development costs to be deducted on preferential terms. Innovative businesses may also consider the IP Box regime, which can provide preferential taxation for qualified income from certain intellectual property rights. These incentives make Poland more attractive for technology, manufacturing, engineering and software companies carrying out development work locally.

Foreign businesses should analyse their Polish CIT position before starting operations, signing contracts, employing staff or creating a local presence. Correct classification of activities at the beginning may help avoid unexpected tax registration, reporting and payment obligations.

→ Corporate Income Tax in Poland

VAT in Poland – Registration, Rates and Compliance

VAT Poland rules are often the first practical tax issue for foreign entrepreneurs selling goods or services in Poland. A foreign business may need VAT registration Poland if it carries out taxable transactions in Poland, stores goods in Poland, imports goods, makes intra-Community transactions, sells locally to Polish customers, or performs activities for which Polish VAT cannot be settled by the buyer under the reverse charge mechanism. The exact obligation depends on the transaction model, the customer type and the place of supply under Polish VAT law.

The standard VAT rate in Poland is 23%. Reduced rates of 8% and 5% apply to selected goods and services, while the 0% rate may apply, among others, to exports, intra-Community supplies and certain international transactions, provided that statutory conditions and documentation requirements are met. The Polish tax portal confirms the 23%, 8%, 5% and 0% VAT rates and the legal basis for applying them.

VAT compliance in Poland usually includes issuing correct invoices, reporting VAT through JPK_V7 files, paying output VAT, deducting input VAT and keeping transaction documentation. From 2026, businesses must also take into account KSeF, Poland’s National e-Invoicing System. Mandatory e-invoicing is being introduced in stages: from 1 February 2026 for the largest taxpayers and from 1 April 2026 for most other VAT-registered businesses in Poland.

Foreign entrepreneurs should also be aware of the split payment mechanism, under which the VAT amount from an invoice may be paid to a separate VAT bank account. In some cases, split payment is mandatory, especially for selected sensitive goods and services listed in Polish VAT regulations. Failure to apply split payment where required may create tax risks for both the buyer and the seller.

Personal Income Tax (PIT) – Rules for Employees and Expats

PIT Poland rules are important both for foreign individuals working in Poland and for employers hiring international staff. Personal income tax Poland applies to employment income, management board remuneration, civil law contracts, business activity and other income earned by individuals. For expats, the key question is whether they are Polish tax residents or non-residents, because tax residents are generally taxed in Poland on worldwide income, while non-residents are taxed only on Polish-source income.

Under the Polish tax scale, income is taxed at 12% up to PLN 120,000 and 32% on the surplus above PLN 120,000. These rules are particularly relevant for employees, managers and contractors unless a different taxation method applies, such as flat tax for certain entrepreneurs.

Tax residence is usually assessed based on personal and economic ties with Poland and the so-called 183-day test. A foreigner may become Polish tax resident if they stay in Poland for more than 183 days in a tax year or have their centre of personal or economic interests in Poland. In cross-border cases, the final result may also depend on the relevant double tax treaty.

Polish PIT law also provides several exemptions and reliefs that may be relevant to employees and expats. These include the return relief for individuals transferring their tax residence back to Poland and the so-called young persons’ relief, which may exempt certain income earned by individuals under the age of 26, subject to statutory limits and conditions.

→ PIT in Poland

→ Polish Tax Residency

Withholding Tax (WHT) – Key Rules for Cross-Border Payments

Withholding tax Poland rules are crucial for foreign investors receiving payments from Polish companies. WHT may apply to outbound payments such as dividends, interest, royalties and selected intangible services. In domestic Polish law, the standard WHT rate is generally 19% for dividends and 20% for interest, royalties and certain service payments made to non-residents.

In practice, WHT Poland dividends and other cross-border payments should always be analysed together with the applicable double tax treaty Poland has concluded with the recipient’s country of residence. A double tax treaty may reduce the WHT rate or provide an exemption, provided that the Polish payer holds proper documentation, including a valid certificate of tax residence, and verifies the beneficial owner and due diligence conditions. Poland has a broad treaty network; current public treaty databases indicate more than 80 double tax treaties.

A special compliance issue is the Polish “pay and refund” mechanism. It may apply when payments subject to WHT made to the same taxpayer exceed PLN 2 million per year. In such cases, the Polish payer may be required to collect WHT at the domestic rate first, while the taxpayer or payer may later apply for a refund, unless an exemption opinion or other statutory protection applies. The Ministry of Finance provides a dedicated WHT section covering the collection and refund system.

Other Key Taxes in Poland You Should Know

Foreign investors should also consider other taxes that may apply depending on the transaction structure, type of asset and business activity. In addition to VAT, CIT, PIT and WHT, the most relevant areas include capital gains tax Poland, PCC tax Poland, property tax Poland, excise duty and selected local taxes.

| Tax | Rate | Who it applies to |

| Capital Gains Tax | 19% | Individuals, investors, funds and shareholders deriving taxable capital gains |

| PCC (Civil Law Transactions Tax) | 0.5–2% | Selected transactions, including share sales, loans and certain civil law agreements |

| Property Tax | Set by municipalities | Owners and holders of real estate located in Poland |

| Excise Tax | Varies | Selected goods, including fuel, alcohol, tobacco, energy products and cars |

For foreign investors, these taxes are often transaction-specific. For example, PCC may be relevant when acquiring shares in a Polish company, real estate tax should be checked before buying or leasing property, and excise duty may materially affect businesses trading in regulated goods.

→ Tax on Civil Law Transactions

Tax Compliance and Reporting Obligations in Poland

Tax reporting Poland is highly digitalised and should be treated as a core part of doing business in Poland, not merely as an accounting formality. Foreign investors often focus on tax rates, but practical compliance obligations — monthly reporting, electronic files, invoice requirements, payment deadlines and disclosure duties — are equally important.

One of the key obligations is JPK SAF-T Poland reporting. VAT taxpayers must submit structured electronic files, including JPK_V7, which combines VAT records and VAT return data. These files allow the tax authorities to verify sales, purchases, VAT rates, deductions and transaction classifications more efficiently.

A major change for 2026 is KSeF Poland, the National e-Invoicing System. KSeF is the system for issuing, receiving and storing structured electronic invoices. According to the official KSeF portal, mandatory KSeF is being introduced from 1 February 2026 and will gradually cover entrepreneurs and invoice issuers in Poland.

Businesses should also consider MDR Poland rules. Mandatory Disclosure Rules require reporting certain tax arrangements to the Head of the National Revenue Administration. The official MDR portal explains that taxpayers and advisers must verify whether an arrangement is a reportable tax scheme and whether they act as a promoter, beneficiary or supporting party.

In addition, businesses must monitor deadlines for tax returns, monthly or quarterly VAT settlements, CIT and PIT advance payments, annual tax returns and other sector-specific filings. Missing a deadline may lead to tax arrears, interest, penalties or additional explanations requested by the tax authorities.

→ SAF-T in Poland→ MDR Regulation

Double Tax Treaties and International Tax Planning

A double tax treaty Poland has concluded with another country may significantly affect the final tax cost of an investment, especially in cross-border structures. Poland has an extensive tax treaty network Poland, covering more than 80 jurisdictions, which helps reduce the risk that the same income will be taxed twice in two different countries. Current treaty databases indicate that Poland has around 85 double taxation agreements in force.

Double tax treaties are particularly important for international taxation Poland because they may determine where a company or individual is tax resident, whether a foreign company has a permanent establishment in Poland, and which country has the right to tax specific income. In practice, DTA provisions often affect Polish withholding tax on dividends, interest, royalties and selected service payments. A treaty may reduce the Polish WHT rate or allow an exemption, but usually only if the payer has proper documentation, including a valid certificate of tax residence, and verifies beneficial ownership and due diligence requirements. Polish WHT guidance confirms that treaty relief and exemptions depend on formal verification and documentation standards.

International tax planning should also take into account global anti-avoidance rules, including BEPS-related measures and Pillar Two. Pillar Two introduces a global minimum effective taxation level of 15% for large multinational groups, generally those with consolidated annual revenues of at least EUR 750 million. Poland implemented the global minimum tax framework in 2025, so by 2026 affected groups should already consider Polish reporting, calculation and top-up tax implications.

These rules are especially relevant for holding companies, cross-border dividend flows, royalty payments, financing structures, intellectual property licensing, management fees and other intangible services. Before applying treaty benefits or restructuring payments through Poland, investors should review the relevant treaty, domestic WHT rules, beneficial owner requirements, substance of the recipient and potential Pillar Two exposure.

How Intertax Can Help You Navigate Polish Tax Law

Working with an experienced tax advisor Intertax can help foreign investors avoid costly mistakes and understand their Polish tax obligations before problems arise. Intertax provides practical tax consultancy services for international clients, including interpretation of Polish tax regulations, tax registration, VAT/CIT/PIT compliance and day-to-day consulting support. We assist businesses at every stage of their presence in Poland — from market entry and transaction planning to ongoing reporting and communication with tax authorities.

Get in touch for a free initial consultation.

FAQ – Polish Tax Law for Foreign Investors

What are the main taxes in Poland?

The main taxes in Poland are VAT, CIT, PIT, WHT and PCC. VAT is a tax on goods and services, usually charged on sales transactions. CIT is corporate income tax paid by companies and other legal entities. PIT is personal income tax paid by individuals, including employees, contractors and sole traders. WHT is withholding tax collected on certain cross-border payments, such as dividends, interest and royalties. PCC is tax on civil law transactions, such as certain share sales, loans and other agreements.

What is the corporate tax rate in Poland in 2026?

The standard corporate income tax rate in Poland in 2026 is 19%. A reduced 9% CIT rate may apply to small taxpayers and certain new businesses, provided that statutory conditions are met.

Do foreign companies need to register for VAT in Poland?

Yes, foreign companies may need to register for VAT in Poland if they make taxable supplies of goods or services in Poland, store goods in Poland, import goods, carry out intra-Community transactions or sell to Polish customers. In some cases, registration may be avoided because the buyer accounts for VAT under the reverse charge mechanism, or because a special EU VAT scheme applies. The applicable threshold and exemptions depend on the type of transaction, customer status and place of supply rules.

How does withholding tax work in Poland?

Withholding tax in Poland applies mainly to outbound payments such as dividends, interest, royalties and selected intangible services paid to non-residents. Polish domestic rates may be reduced or eliminated under a double tax treaty, provided that the payer has proper documentation and verifies the beneficial owner and due diligence requirements. For payments exceeding PLN 2 million per year to the same taxpayer, the Polish Pay & Refund mechanism may require tax to be withheld first, with the possibility of applying for a refund or using available statutory protections.

Is Poland a good country for business taxes?

Poland can be attractive from a business tax perspective, especially for small companies eligible for the 9% CIT rate, innovative businesses using the IP Box regime, and investors benefiting from support instruments such as Special Economic Zones or the Polish Investment Zone. At the same time, Polish tax compliance is relatively complex and includes VAT reporting, SAF-T/JPK files, KSeF e-invoicing, withholding tax due diligence and documentation obligations. For foreign investors, Poland is often a competitive location, but the tax structure should be planned carefully before starting operations.

Contact our expert to find out how to optimally organize your company’s entry into Poland.