Executive Summary

The General Anti-Avoidance Rule (GAAR) in Poland allows the tax authority to deny tax benefits from artificial arrangements that are formally legal but inconsistent with the purpose of tax law.

For foreign businesses, the practical risk is not only a tax reassessment. GAAR can affect restructurings, holding structures, financing flows, dividend planning, asset transfers and other arrangements where tax benefit is one of the main drivers.

A defensible structure should be supported before implementation by business-purpose documentation, substance, decision records, financial analyses and, where appropriate, a protective opinion or specialist tax review.

What Is the General Anti-Avoidance Rule (GAAR) in Poland?

GAAR in Poland is an anti-avoidance rule in the Polish Tax Ordinance that allows the Head of the National Revenue Administration to deny tax benefits from artificial transactions. It applies where a formally legal arrangement mainly seeks a tax benefit contrary to the purpose of tax law.

In business terms, GAAR is not a rule against every form of tax planning. It is a rule against using legal form to obtain a tax result that the tax law was not intended to provide. This distinction matters for foreign groups: choosing a tax-efficient structure is not automatically abusive, but a structure with no credible business reason can become vulnerable.

Polish GAAR has applied since 15 July 2016. The rules were later changed, including from 1 January 2019, to align the Polish system more closely with broader EU anti-avoidance standards and to extend practical consequences such as additional tax liability in relevant cases.

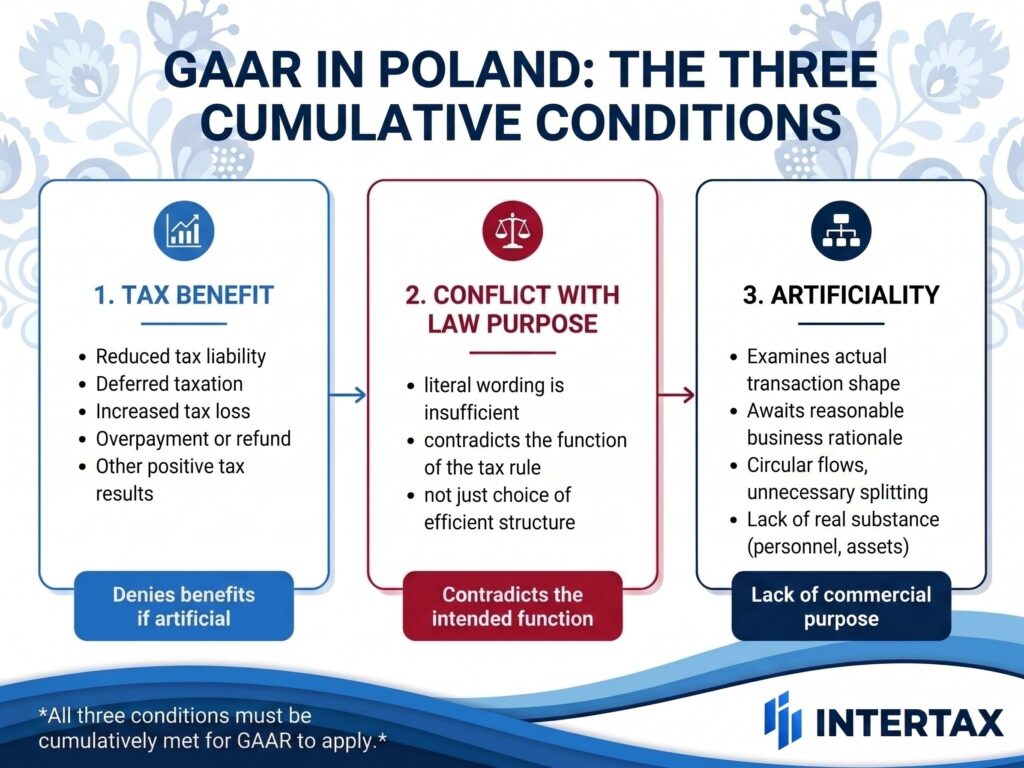

Three Conditions for GAAR to Apply

Polish GAAR is based on cumulative conditions. In simplified terms, the tax authority must identify a tax benefit, show that the benefit is inconsistent with the object or purpose of tax law, and establish that the manner of action was artificial.

1. A tax benefit. This can include a reduced tax liability, deferred taxation, an increased tax loss, an overpayment, a refund or another favourable tax result.

2. Conflict with the purpose of tax law. It is not enough that the taxpayer followed the literal wording of a rule. The authority considers whether the benefit contradicts the function that the tax rule was meant to serve.

3. Artificiality. The key question is whether a reasonably acting entity, guided by lawful and predominantly economic reasons other than the disputed tax benefit, would have chosen the same structure.

All three elements matter. If a transaction has a real commercial purpose, operational substance and a defensible business rationale, GAAR risk is lower. The structure may still need review, but the mere fact that it is tax-efficient does not make it artificial.

Examples of arrangements that are not automatically artificial include choosing a lower-tax legal form where that form fits the business, using a statutory exemption that the taxpayer genuinely qualifies for, or centralising functions in a holding company that performs real decision-making, financing or management activity.

What Counts as an “Artificial Transaction” Under Polish GAAR?

Artificiality is the most practical part of the GAAR test. The Head of KAS examines the actual shape of the transaction, not only the documents that describe it. A structure may look legally correct but still raise questions if its steps make little business sense without the tax result.

Risk indicators include unnecessary splitting of operations, circular flows, short-lived transactions created only to secure a tax effect, involvement of intermediary entities with no real economic role, a lack of personnel, assets or decision-making substance, and economic risk that is disproportionate to the non-tax benefits.

By contrast, a holding or financing structure is not artificial merely because it produces a tax advantage. A group treasury company, IP holding company or acquisition vehicle may be defensible where it has decision-makers, documented functions, real financial exposure, governance records and a business purpose that exists independently from the tax saving.

What Tax Benefits Can GAAR Deny?

GAAR can deny a broad range of tax benefits, including the non-arising of a tax liability, reduction of tax, deferral of payment, generation or increase of a tax loss, overpayment, refund or increased refund.

For foreign businesses, this means GAAR can affect more than one line in a tax model. It may change the timing of taxation, the amount of taxable income, the availability of losses, the treatment of deductions, or the tax effect of a restructuring.

Important scope note: the Polish Tax Ordinance GAAR should not be presented as a standard VAT GAAR. Public Ministry of Finance guidance states that the clause is not applied to VAT; VAT has separate anti-abuse concepts and mechanisms. This article therefore focuses on GAAR under the Tax Ordinance, with income tax and other non-VAT tax consequences assessed case by case.

Who Enforces GAAR in Poland? The Role of the Head of KAS

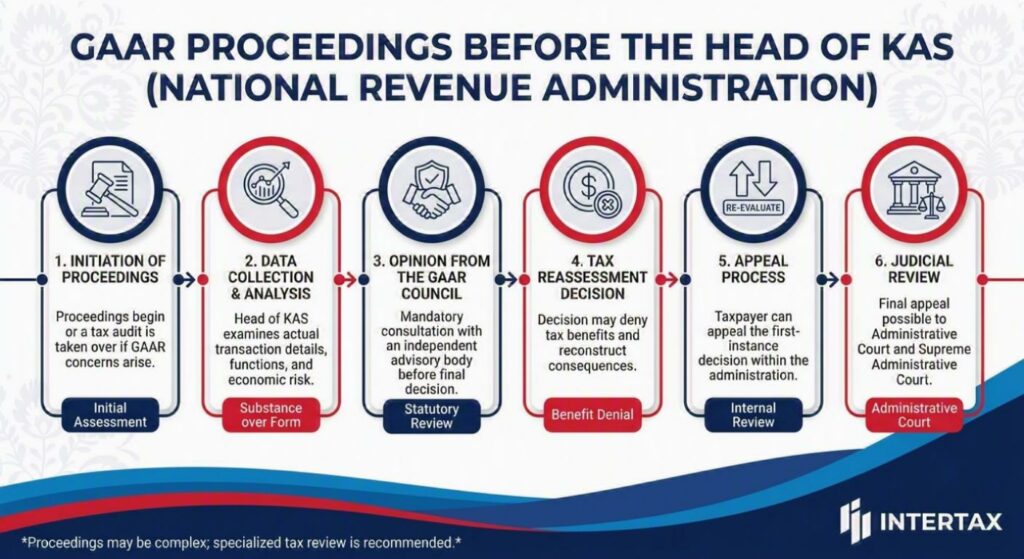

GAAR is applied by the Head of the National Revenue Administration, known in Polish as the Szef Krajowej Administracji Skarbowej or Head of KAS. This is a central tax authority, not an ordinary local tax office.

The Head of KAS may initiate GAAR proceedings or take over an ongoing tax audit or tax proceeding if the authority considers that the GAAR clause may be relevant. In a GAAR decision, the authority may determine the tax consequences as if the taxpayer had performed an appropriate transaction that a reasonable entity would have chosen for legitimate business reasons.

If the tax benefit was the sole purpose of the action, the authority may determine the tax consequences as if the action had not been performed. This is why GAAR analysis must look beyond legal form and examine what the group would have done without the tax benefit.

The Head of KAS also acts as the decision-maker in the first instance. A taxpayer can appeal the decision under the general rules of the Tax Ordinance and may ultimately challenge the case before administrative courts, but that process can be lengthy and fact-intensive.

GAAR Proceedings – Step by Step

1. Opening or takeover of the case. The Head of KAS may initiate a GAAR proceeding directly or take over an existing tax case where avoidance concerns arise.

2. Identification of the tax benefit and relevant transaction. The authority analyses what tax result was achieved and which steps produced it.

3. Assessment of artificiality and purpose. The authority tests whether a reasonable entity would have acted in the same way for lawful economic reasons other than the disputed tax benefit.

4. Determination of the appropriate tax consequences. If GAAR applies, the authority may reconstruct the tax result by reference to an appropriate transaction or, in sole-purpose cases, by disregarding the action.

5. Decision and potential additional tax liability. A GAAR decision may be combined with an additional tax liability under the Tax Ordinance. The rate depends on the legal basis and the type of tax consequence. Because rates can be nuanced, the penalty wording should be confirmed before publication for the specific article period.

6. Appeal and court review. The taxpayer may appeal from the Head of KAS decision and later seek administrative court review.

Practical note on evidence: the article should not say that the legal burden of proof always rests on the taxpayer. A safer formulation is that the authority must establish the GAAR conditions, but the taxpayer should be ready to prove the commercial rationale with contemporaneous documentation. In practice, weak business-purpose evidence can make a defence much harder.

GAAR vs. Legitimate Tax Planning – Where Is the Line?

The line between legitimate tax planning and tax avoidance is not drawn by tax savings alone. A business may choose a lawful structure that reduces tax, provided the structure reflects real commercial choices and does not contradict the purpose of the relevant tax rules.

Legitimate planning may include choosing between a branch and a subsidiary, using available exemptions where statutory conditions are genuinely met, financing a Polish company through a commercially justified mix of debt and equity, or reorganising a group to simplify management and reporting.

Higher-risk examples include inserting an intermediary company shortly before a dividend payment where it has no substance, creating circular financing with no economic exposure, splitting a transaction into steps that cancel each other out, or transferring assets briefly only to trigger a tax result.

Borderline cases are common. A group restructuring may reduce tax and still be defensible if it centralises real functions, improves financing access, reduces operational risk, separates business lines, or supports an acquisition. The same restructuring becomes riskier if those reasons are invented after the fact or are not visible in board papers, financial models and operational reality.

How to Protect Your Business from GAAR Risk in Poland

GAAR protection starts before implementation. The strongest file is usually built when the transaction is being designed, not after the tax authority asks questions.

Prepare business-purpose documentation. Record why the structure is needed, what alternatives were considered, what non-tax benefits are expected, and who made the decision. Board minutes, financial models, legal memoranda, operational analyses and emails can all matter.

Test the arrangement against the GAAR criteria. A pre-implementation review should ask whether the structure creates a tax benefit, whether the benefit is consistent with the purpose of the relevant rules, whether each step has a business role, and whether a reasonable entity would choose the same arrangement without the tax benefit.

Consider formal instruments. An individual tax ruling can help show that the taxpayer sought clarity, but it does not fully protect against GAAR. For high-risk arrangements, the dedicated instrument is a protective opinion from the Head of KAS. For related-party pricing issues, an Advance Pricing Agreement may also reduce transfer pricing risk, although it is not a GAAR shield for every element of a structure.

Align GAAR work with transfer pricing and tax governance. Related-party transactions should be priced and documented consistently. For practical context, see PolishTax’s guide to transfer pricing in Poland and Intertax tax consultancy support.

GAAR and SAAR – Key Differences

GAAR is a general anti-avoidance rule. SAAR means specific anti-avoidance rules, which target narrower types of tax benefits or transactions. In Poland, SAAR-type rules are particularly relevant in withholding tax, dividend, interest, royalty and beneficial ownership contexts.

The two concepts can interact. A transaction may first be tested under a specific anti-abuse rule, but the broader GAAR analysis may still be relevant if the structure is artificial and one of its main purposes is to obtain a tax benefit contrary to the purpose of tax law.

|

GAAR |

SAAR |

|

|

Scope |

General anti-avoidance clause; potentially broad transaction types, subject to statutory exclusions. |

Specific anti-avoidance rules for defined areas, e.g. WHT exemptions, dividends, interest and royalties. |

|

Legal basis |

Tax Ordinance Act, especially Art. 119a and related Division IIIA rules. |

CIT / PIT provisions and specific tax rules, depending on the benefit. |

|

Authority |

Head of KAS. |

Usually ordinary tax authorities competent for the specific tax area; exact authority depends on the procedure. |

|

Consequence |

Denial of tax benefit, reconstructed tax consequences, possible additional tax liability. |

Denial of exemption/preference, tax assessment and interest; penalties depend on the case. |

|

In force |

Since 2016. |

Many key modern anti-abuse restrictions apply from 2016 or later, depending on the provision. |

Is your tax structure GAAR-compliant? Contact Intertax for a professional review of your transactions and documentation.

People Also Ask / FAQ

What is the GAAR clause in Poland?

The GAAR clause in Poland is a Tax Ordinance anti-avoidance rule that lets the Head of KAS deny tax benefits from artificial arrangements. It applies where a formally legal transaction mainly produces a tax benefit contrary to the purpose of tax law.

When does GAAR apply in Poland?

GAAR applies when three conditions are met together: the taxpayer obtains a tax benefit, the benefit conflicts with the object or purpose of tax law, and the arrangement is artificial when tested against how a reasonable business would act.

What is the penalty for tax avoidance under GAAR in Poland?

A GAAR decision may lead to additional tax liability under the Tax Ordinance. Some GAAR-related consequences can be discussed by reference to a 40% rate, but penalty calculation is nuanced and must be confirmed for the tax type and facts before publication.

Can a tax ruling protect against GAAR in Poland?

An individual tax ruling does not fully protect against GAAR. It may support good-faith positioning, but the dedicated GAAR protection instrument is a protective opinion issued by the Head of KAS for the described arrangement.

What is the difference between GAAR and SAAR in Poland?

GAAR is a general anti-avoidance rule for artificial tax-benefit arrangements. SAAR rules are specific anti-avoidance provisions that apply to defined benefits or taxes, such as withholding tax exemptions for dividends, interest or royalties.

Sources Used

-

Ministry of Finance / podatki.gov.pl GAAR page: https://podatki-arch.mf.gov.pl/abc-podatkow/klauzula-przeciwko-unikaniu-opodatkowania/

-

ELI record for Dz.U. 2026 poz. 622 – consolidated Tax Ordinance Act: https://eli.gov.pl/eli/DU/2026/622/ogl

-

Dziennik Ustaw 2026, item 825 – 29 May 2026 amendment to Tax Ordinance: https://dziennikustaw.gov.pl/DU/2026/825

-

Council Directive (EU) 2016/1164 consolidated text, Article 6: https://eur-lex.europa.eu/legal-content/EN/TXT/HTML/?uri=CELEX:02016L1164-20220101

-

Ministry of Finance WHT page for SAAR/WHT context: https://www.podatki.gov.pl/pozostale/wht-withholding-tax-podatek-u-zrodla

-

PolishTax Transfer Pricing guide: https://polishtax.com/transfer-pricing-in-poland-what-you-need-to-know/

-

PolishTax CIT guide: https://polishtax.com/information/polish-tax-law/cit/

-

PolishTax Tax Consultancy service page: https://polishtax.com/services/tax-consutancy/

-

PolishTax WHT guide: https://polishtax.com/information/polish-tax-law/withholding-tax/