Executive Summary

Specific Anti-Avoidance Rules, or SAAR, are targeted Polish tax rules that may deny withholding tax exemptions where a transaction or structure is artificial and one of its main purposes is to obtain a tax benefit. For foreign groups, SAAR is especially relevant to dividends, interest and royalties paid by Polish companies to related entities abroad. In practice, a WHT exemption is safer when the recipient has real economic substance, beneficial owner status where required, and a documented business rationale for the structure.

Polish SAAR provisions are specific anti-avoidance rules linked to particular tax preferences. In the withholding tax area, the key provision is art. 22c of the Polish Corporate Income Tax Act. This rule may prevent the use of statutory WHT exemptions if the exemption would be used contrary to the purpose of the provision and the arrangement is artificial.

SAAR should be understood as a targeted tool. It does not replace the general anti-avoidance rule, and it does not automatically apply to every cross-border payment. It focuses on statutory exemptions, including the dividend exemption under art. 22 ust. 4 CIT and the interest and royalties exemption under art. 21 ust. 3 CIT.

The concept is closely connected with EU anti-abuse policy, including the Parent-Subsidiary Directive and the rules introduced to prevent the use of non-genuine arrangements. For a foreign CFO or tax director, the key question is practical: does the receiving company genuinely perform a business role, or is it mainly a conduit used to secure a Polish WHT exemption?

A non-genuine or artificial arrangement is not defined by a single formal defect. Polish tax authorities may look at the wider picture: commercial reasons, economic substance, decision-making, personnel, office presence, risk control, contractual terms and the actual flow of funds. The absence of one element is not always decisive, but a combination of weak substance and tax-driven design may create SAAR risk.

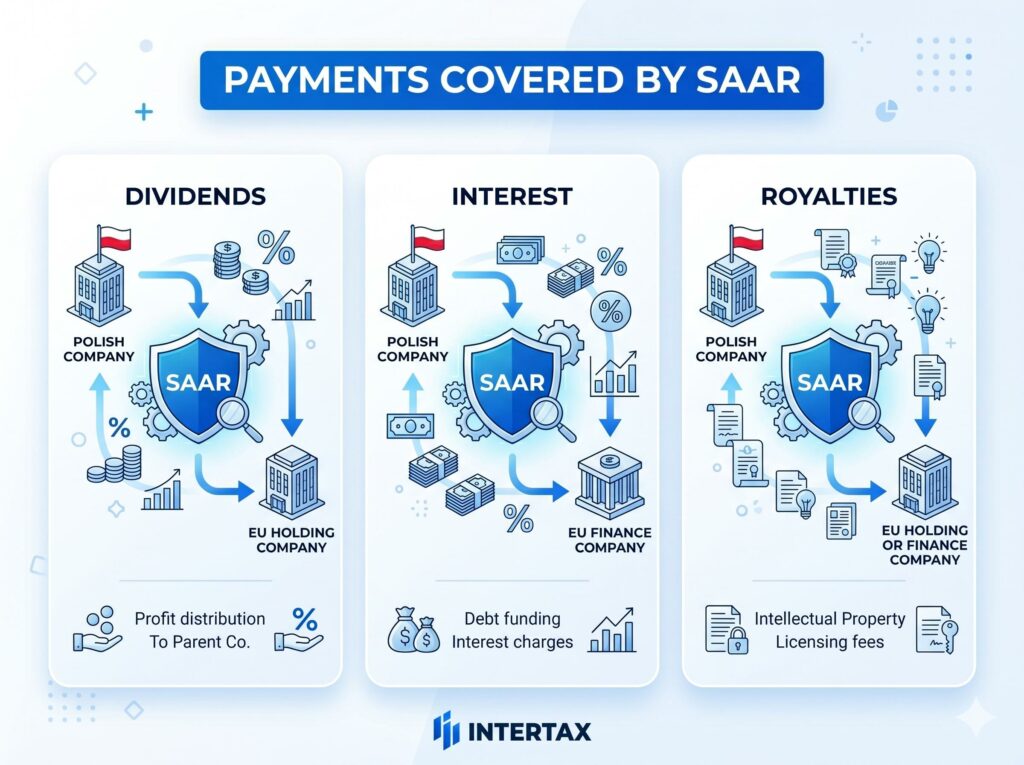

What Payments Are Covered by SAAR?

In the Polish WHT context, SAAR is relevant mainly to three categories of cross-border payments: dividends, interest and royalties. These payments are often made within international groups, for example when a Polish subsidiary distributes profit to an EU parent company, pays interest under intra-group financing, or pays royalties for intellectual property.

|

Payment type |

Exemption basis |

SAAR provision |

|

Dividends |

Parent-Subsidiary Directive framework; art. 22 ust. 4 CIT |

Art. 22c CIT may block the exemption |

|

Interest |

Interest and Royalties Directive framework; art. 21 ust. 3 CIT |

Art. 22c CIT may block the exemption |

|

Royalties |

Interest and Royalties Directive framework; art. 21 ust. 3 CIT |

Art. 22c CIT may block the exemption |

A practical distinction is important here. SAAR in art. 22c CIT directly addresses statutory exemptions. Relief under a double tax treaty is a separate route and depends on treaty provisions, domestic WHT rules, certificates, beneficial owner analysis and anti-abuse concepts that may apply under the treaty or Polish law. In other words, SAAR should not be mechanically equated with treaty relief, but a treaty claim is not immune from anti-abuse scrutiny.

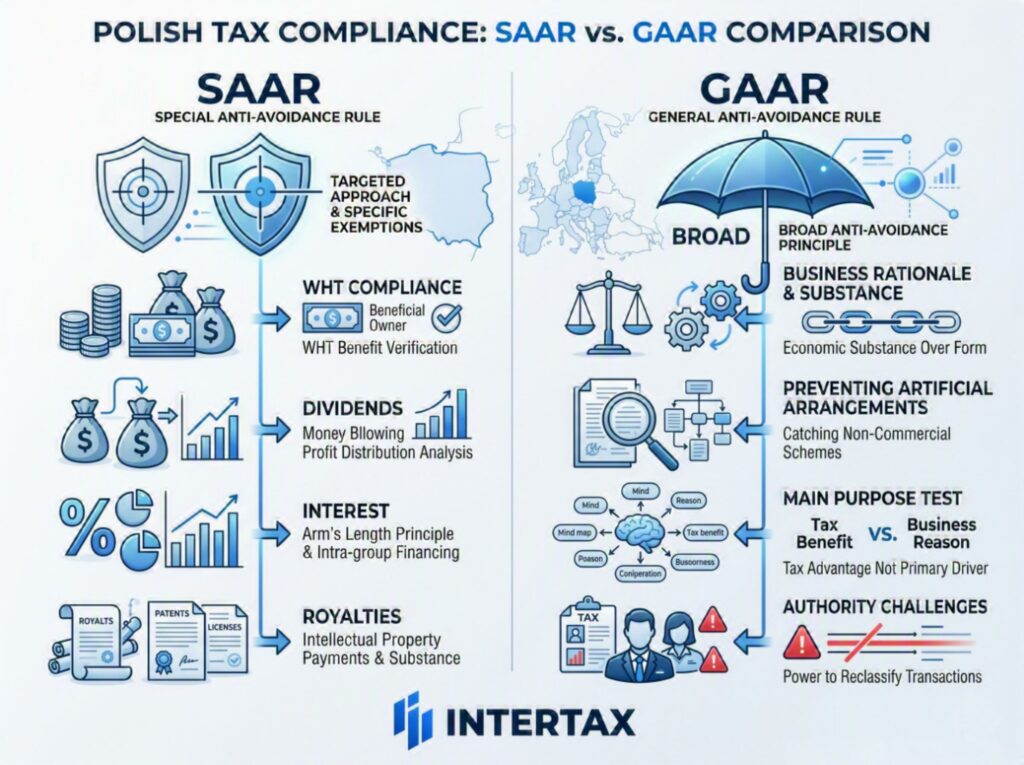

SAAR vs. GAAR: Key Differences

SAAR and GAAR are often discussed together, but they are not the same tool. GAAR is the general anti-avoidance rule under the Polish Tax Ordinance. SAAR is a specific rule embedded in the CIT Act for particular exemptions. The distinction matters because it affects procedure, competent authority and the type of transaction being challenged.

|

Criterion |

GAAR |

SAAR |

|

Scope |

Potentially broad anti-avoidance tool for tax benefits. |

Targeted rule for specific statutory exemptions, including WHT exemptions. |

|

Legal basis |

Art. 119a of the Tax Ordinance. |

Art. 22c CIT, linked to art. 21 ust. 3 and art. 22 ust. 4 CIT. |

|

Authority |

Proceedings connected with the Head of the National Revenue Administration. |

Can be considered by the tax authority handling the WHT case. |

|

Threshold |

Do not rely on the old PLN 100,000 threshold without current legal confirmation. |

No separate statutory monetary threshold in art. 22c CIT. |

|

Typical WHT relevance |

Broader tax avoidance cases. |

Denial of a dividend, interest or royalty exemption. |

For broader context on Polish withholding tax rules, see the Polishtax guide to withholding tax in Poland:

When Does SAAR Apply? The Main Purpose Test

SAAR may apply when the use of the exemption is contrary to the purpose of the relevant CIT provision and the main purpose, or one of the main purposes, of the arrangement is to obtain the tax exemption. The rule also looks at artificiality. This means that the authorities are not limited to checking whether formal conditions are written into the documents. They may ask whether the structure makes commercial sense.

The typical risk indicators are practical rather than purely formal. First, the intermediary company has little or no economic substance: no personnel, no office, no meaningful operating costs and no real management activity. Second, the company does not control or use the income in a genuine way and passes funds onward under back-to-back arrangements. Third, the holding, financing or licensing structure was created mainly to obtain a Polish WHT exemption rather than to serve a defensible business purpose.

Consider a simple example. A Polish subsidiary pays a dividend to an EU parent company. On paper, the parent meets formal participation exemption conditions. In practice, however, the parent has no employees, no real office, no independent management decisions and immediately transfers the funds to a non-EU entity. If the facts show that the EU company was inserted mainly to obtain the Polish dividend exemption, the tax authorities may seek to deny the exemption under SAAR.

The opposite case is not simply a company with a large office or hundreds of employees. A holding company may still be genuine if it has a real strategic role, board-level decision-making, adequate resources, risk control and documented commercial reasons for holding the Polish investment. The evidence must match the role the company claims to perform.

Consequences of SAAR Application

If SAAR applies, the Polish WHT exemption is denied. The Polish payer may then be required to withhold tax at the domestic statutory rate, unless another valid basis for relief applies. Under Polish CIT rules, the standard domestic WHT rate is generally 19% for dividends and 20% for interest and royalties.

The practical risk often sits with the Polish payer. If the payer did not withhold WHT and the tax authority later challenges the exemption, the payer may face a tax arrears exposure, interest and procedural consequences. In more serious cases, fiscal penal liability may also need to be considered. That issue depends on the facts and should be reviewed separately.

SAAR risk also affects timing and cash flow. If the payment falls under the Polish pay-and-refund mechanism, the payer may need to collect tax first when the statutory threshold is exceeded, unless a valid route is available to apply the preference at source. The recipient or payer may later seek a refund, but the refund process requires evidence.

How to Protect Your Structure Against SAAR: Compliance Checklist

There is no single document that makes a structure automatically SAAR-proof. The safer approach is to align legal form, economic reality and documentation before the payment is made.

-

Confirm the legal basis for the WHT preference and identify whether the payment relies on art. 21 ust. 3 CIT, art. 22 ust. 4 CIT or a double tax treaty.

-

Document the commercial rationale for the holding, financing or licensing structure.

-

Verify the recipient’s economic substance: office, personnel, management, operating costs, functions and risks.

-

Assess beneficial owner status where relevant, especially for interest and royalties and for broader WHT due diligence.

-

Prepare board minutes, agreements, transfer flow documentation and evidence of decision-making before the payment.

-

Check whether the PLN 2 million pay-and-refund threshold applies to payments to the same taxpayer in the relevant year.

-

Consider applying for an opinion on applying WHT preferences where the structure and payment profile justify it.

-

Keep the payer’s due diligence file consistent with the scale and nature of the transaction.

For foreign groups, the most common mistake is treating WHT as a formality handled only at payment date. SAAR analysis should be performed earlier, when the group designs or changes its holding, financing or IP structure. Once the funds have moved and the documents are incomplete, defending the exemption becomes harder.

SAAR and the Pay-and-Refund Mechanism

Polish WHT rules include a pay-and-refund mechanism for certain payments exceeding PLN 2,000,000 to the same taxpayer in the relevant tax year. In broad terms, if the threshold is exceeded, the payer may be required to collect WHT at the domestic rate first, even where an exemption or reduced rate may ultimately be available.

The rules include mechanisms that may allow preference at source, such as a payer statement or an opinion on applying preferences, provided the statutory conditions are met. However, these tools do not remove the need to verify whether the recipient and arrangement are genuine. If SAAR concerns exist, the authority may still examine the facts behind the exemption.

Where tax has been withheld and a refund is requested, the applicant should be prepared to evidence both formal eligibility and the absence of artificiality. This may include residence documents, corporate documents, payment evidence, contracts, statements on beneficial ownership and evidence of real business activity.

FAQ: Specific Anti-Avoidance Rules in Poland

What is the difference between SAAR and GAAR in Poland?

GAAR is the general anti-avoidance rule in the Polish Tax Ordinance. SAAR is a specific anti-avoidance rule in the CIT Act that may deny particular statutory exemptions, including WHT exemptions for dividends, interest and royalties.

Can SAAR block a WHT exemption on dividends paid to an EU parent company?

Yes. If the dividend exemption under art. 22 ust. 4 CIT is used through an artificial arrangement and one of the main purposes is to obtain the exemption, art. 22c CIT may block the exemption.

What is a non-genuine transaction under Polish tax law?

In this context, a non-genuine or artificial arrangement is one that lacks sufficient economic justification and is mainly tax-driven. Indicators may include lack of substance, lack of real decision-making, conduit flows and no defensible commercial reason for the structure.

Does SAAR apply to payments under double tax treaties?

Art. 22c CIT directly blocks specific statutory exemptions. Treaty relief is a separate route and should be analysed under the relevant treaty, domestic WHT rules and applicable anti-abuse principles. The safer position is not to assume that treaty relief is free from anti-abuse review.

What documentation do I need to avoid SAAR application in Poland?

A good file should include the legal basis for the preference, corporate and tax residence documents, contracts, payment evidence, beneficial owner analysis where relevant, substance evidence and a clear written explanation of the business purpose of the structure.

Next Steps

SAAR risk is best assessed before the payment is made. If your Polish company pays dividends, interest or royalties to a foreign related entity, review the structure, evidence and WHT procedure in advance. Not sure if your payment structure is SAAR-proof? Contact our tax advisors for a review.

Sources

-

Polish Corporate Income Tax Act, consolidated text, ISAP: https://isap.sejm.gov.pl/isap.nsf/download.xsp/WDU19920210086/U/D19920086Lj.pdf

-

Polish Tax Ordinance, ISAP: https://isap.sejm.gov.pl/isap.nsf/download.xsp/WDU19971370926/U/D19970926Lj.pdf

-

Ministry of Finance WHT page: https://www.podatki.gov.pl/pozostale/wht-withholding-tax-podatek-u-zrodla/

-

Ministry of Finance General Interpretation DD9.8202.1.2024: https://www.gov.pl/web/finanse/interpretacja-ogolna-nr-dd9820212024-ministra-finansow-z-dnia-15-listopada-2024-r-dotyczaca-niektorych-warunkow-stosowania-zwolnienia-okreslonego-w-art-22-ust-4-ustawy-o-podatku-dochodowym-od-osob-prawnych

-

Council Directive (EU) 2015/121: https://eur-lex.europa.eu/legal-content/EN/TXT/PDF/?uri=CELEX:32015L0121

-

Council Directive 2003/49/EC: https://eur-lex.europa.eu/legal-content/EN/TXT/?uri=CELEX:32003L0049

-

CJEU Nordcurrent group, C-228/24: https://eur-lex.europa.eu/legal-content/EN/TXT/PDF/?uri=CELEX:62024CJ0228